Analysis by Hannah Smith

This year has been strong for Australia, which has outpaced many regions in hotel performance growth. More noteworthy is the way in which Australia has achieved that growth.

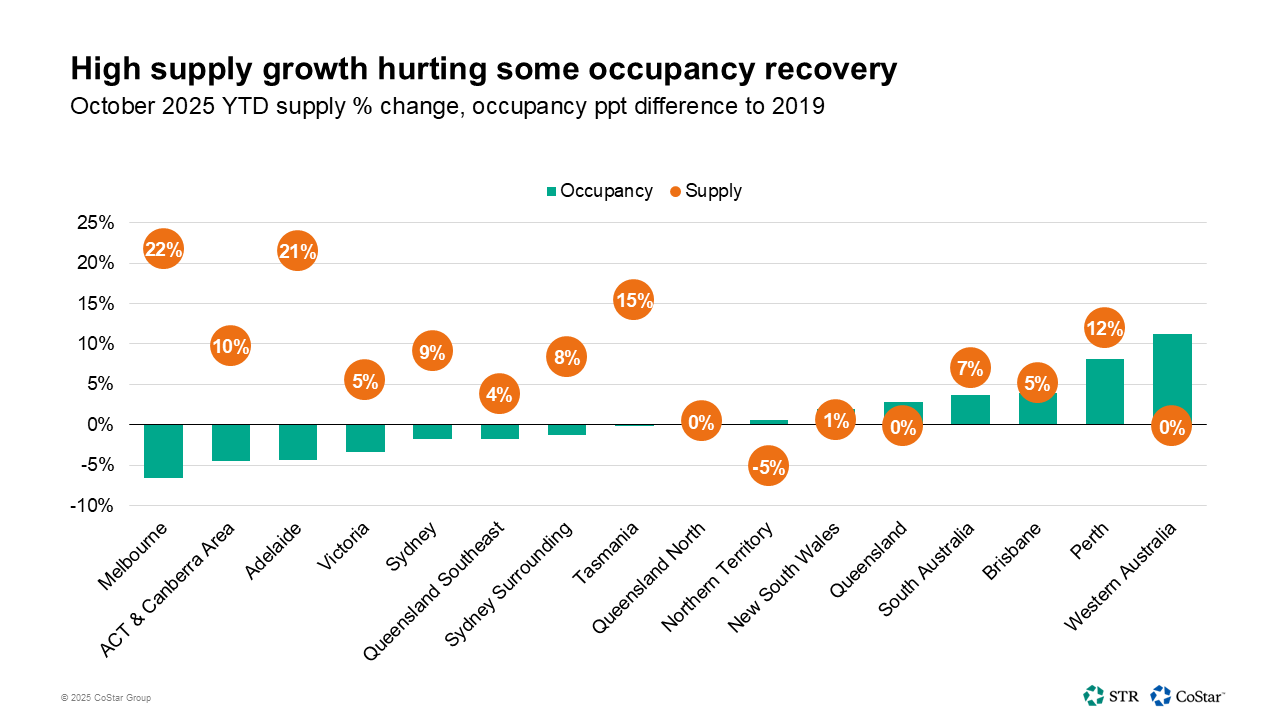

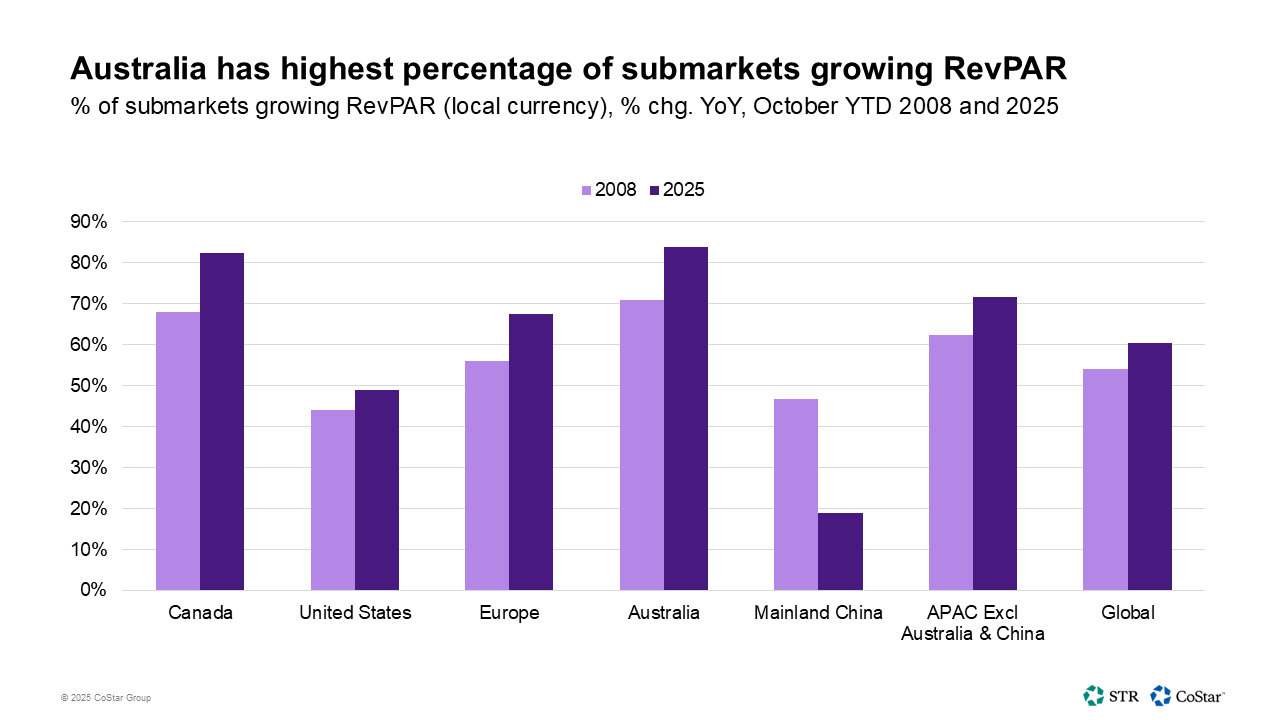

Compared to other Asia Pacific countries, Australia has reported the most widespread growth, with 84% of the country’s submarkets showing an increase in revenue per available room (RevPAR) through the first ten months of the year.

Further, among the world’s 15 largest countries based on hotel room supply, Australia ranks seventh in YTD RevPAR growth, outpacing countries such as Canada, Italy, the U.K., and the U.S.

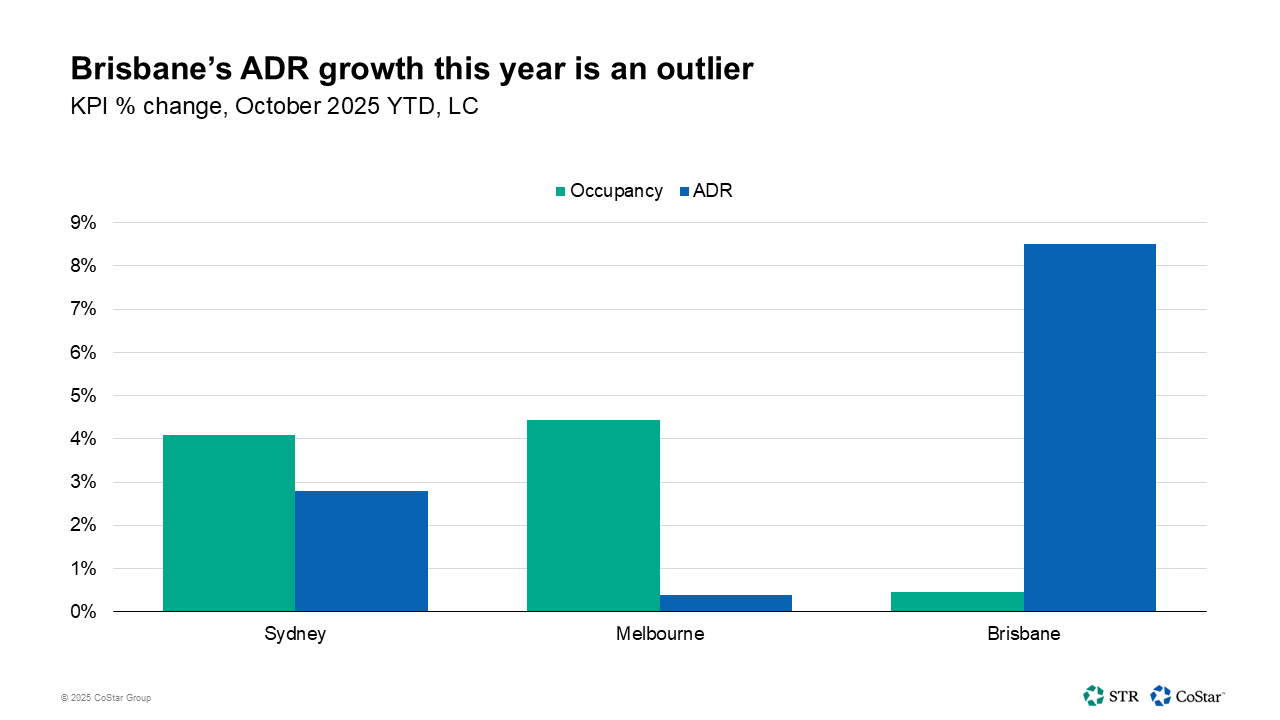

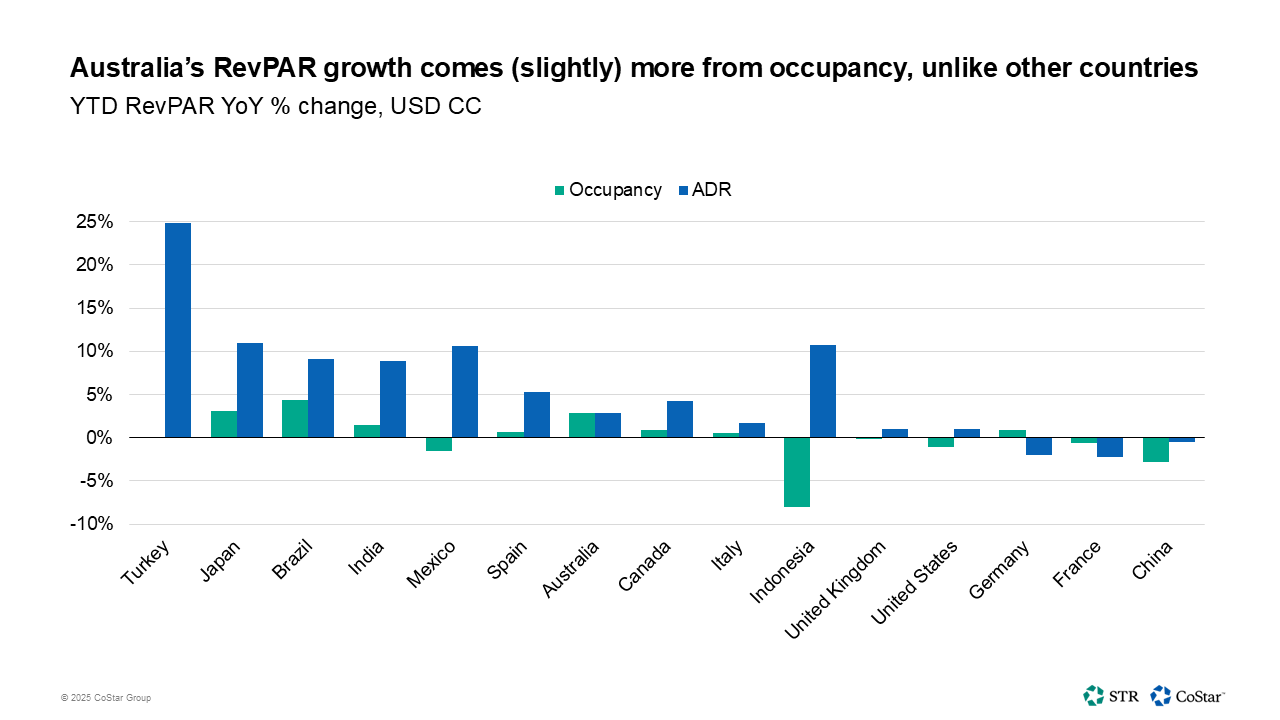

What stands out most, however, is Australia is the only one of those countries driving RevPAR increases through occupancy as opposed to average daily rate (ADR). In nearly every world region, hotels are relying more on pricing power to bolster the top line.

Compression stories are different across markets

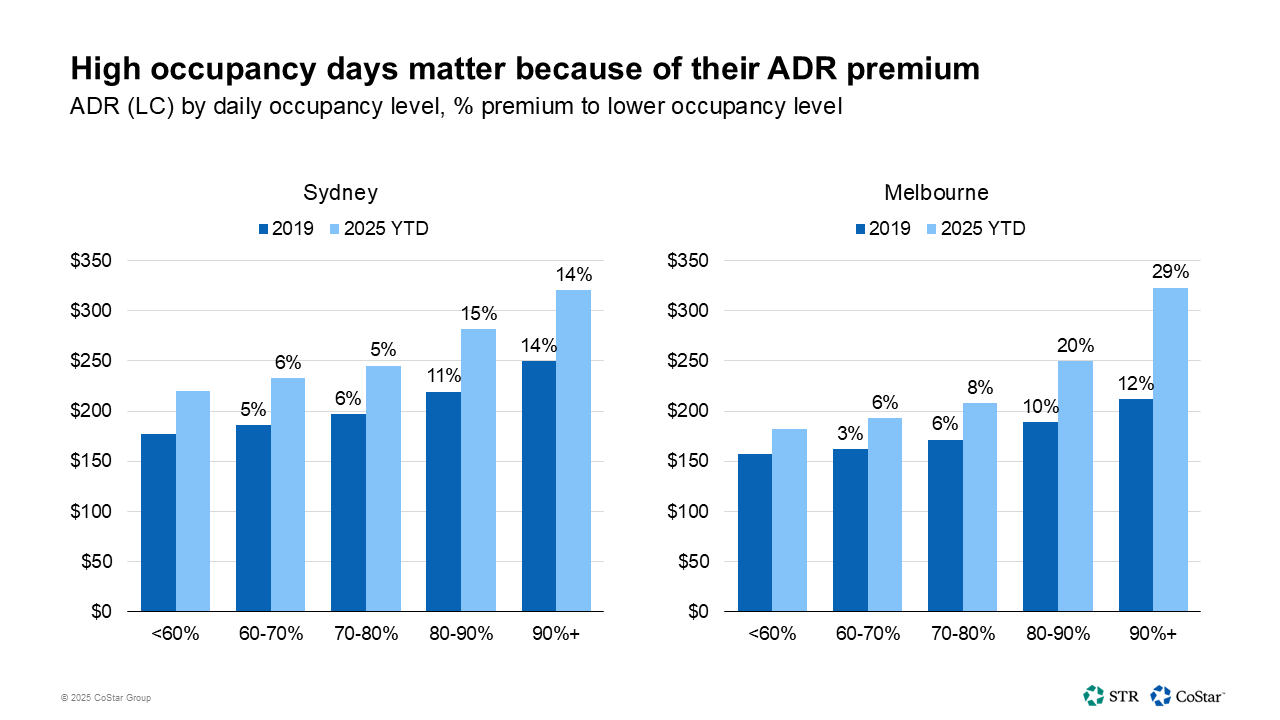

Historically, compression nights were important for major markets in Australia, with 20% of days in Sydney and Melbourne reporting a 90%+ occupancy in 2019.

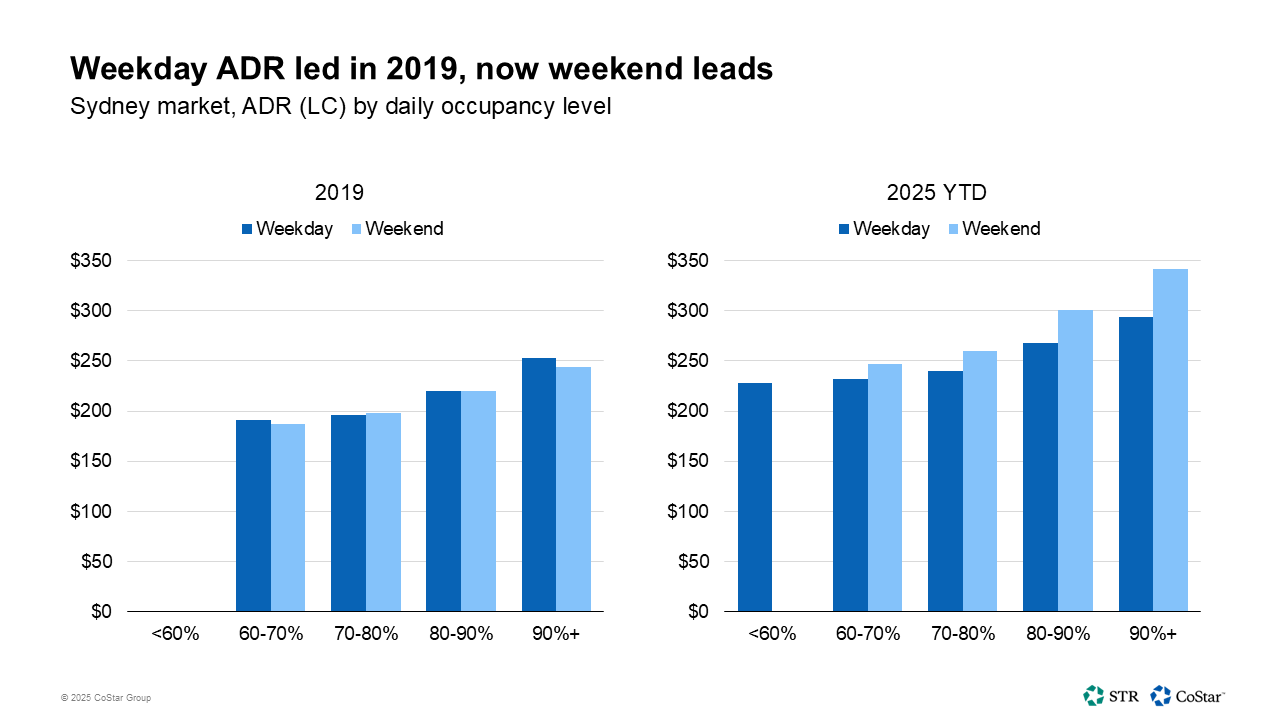

There’s been some rebound in compression in Sydney, with over half of days above an 80% occupancy and 13% of days above the 90% threshold. ADR premiums have also remained relatively stable for Sydney – when looking between 60%-80% occupancy, there’s a 5-6% jump in ADR for each 10-percentage point increase in occupancy. Above 80%, that ADR variance increases to between 12-15%.