Analysis by Isaac Collazo, Chris Klauda

All financial figures in U.S. dollar constant currency.

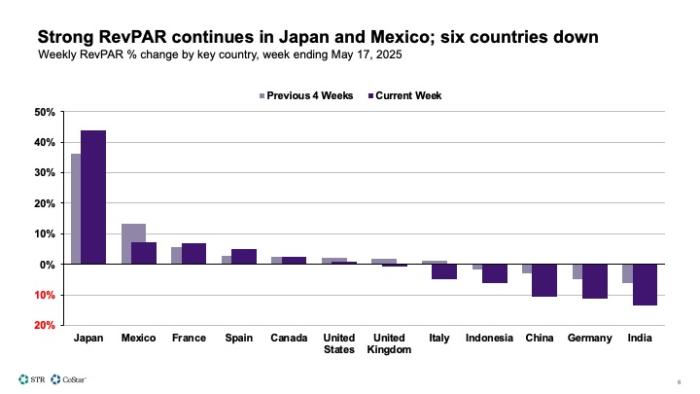

Highlights

- Weekend nights and non-Top 25 Markets drove U.S. RevPAR

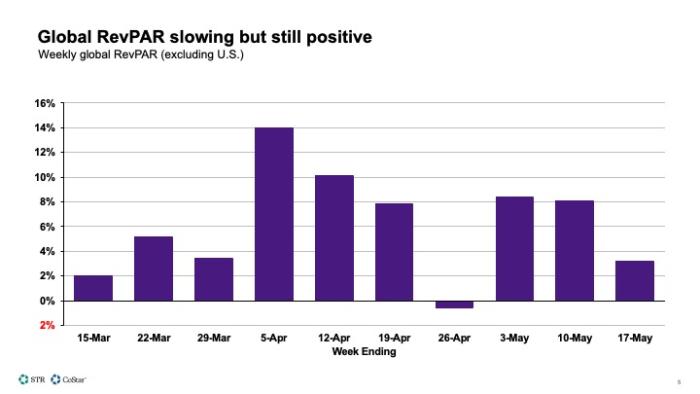

- Global RevPAR slowed but remained positive

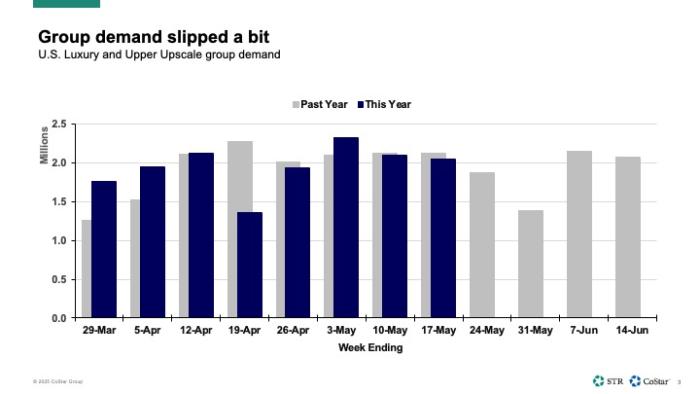

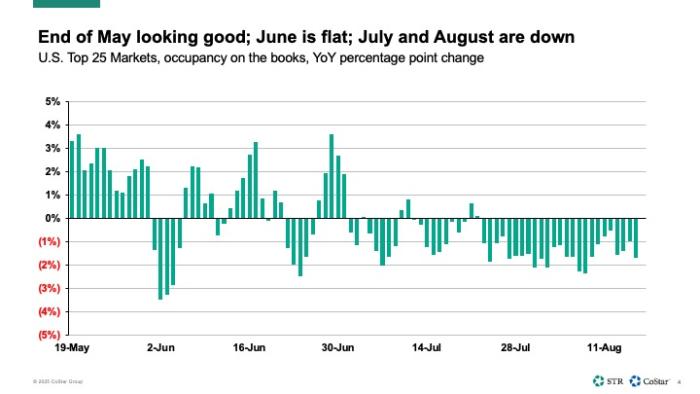

- Mixed signals ahead for summer

Weekends made up for lackluster weekday performance

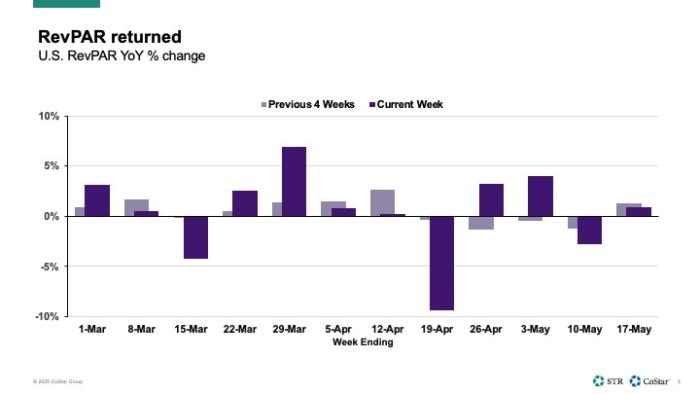

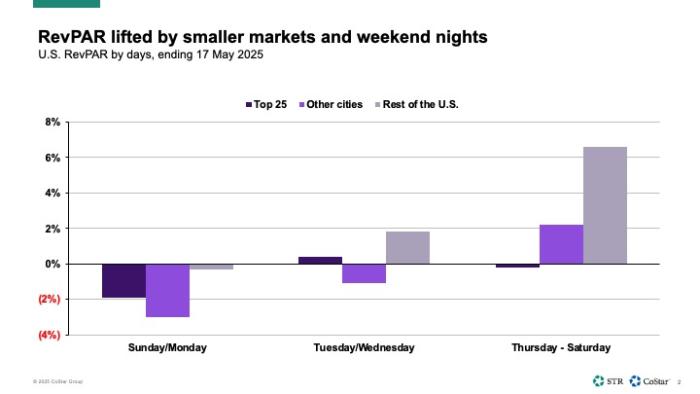

U.S. hotels posted a modest advance in the week ending 17 May with a strong ending offsetting lackluster performance at the beginning. Revenue per available room (RevPAR) rose 0.9%, lifted by a 1.3% gain in average daily rate (ADR) as occupancy fell. RevPAR on Thursday through Saturday increased 2.4% with Friday on top at +3.3%. Tuesday/Wednesday was flat (+0.4%), and the start of the week was down (-1.7). This is notable because last week, it was the weekend that saw the largest loss. It is difficult to pinpoint the cause of this weekend flip, but it's possible that a shift in high school and college graduations occurred due the later start of the semester after the Christmas/New Year holidays.