Analysis by Isaac Collazo

All financial figures in U.S. dollar constant currency.

Highlights

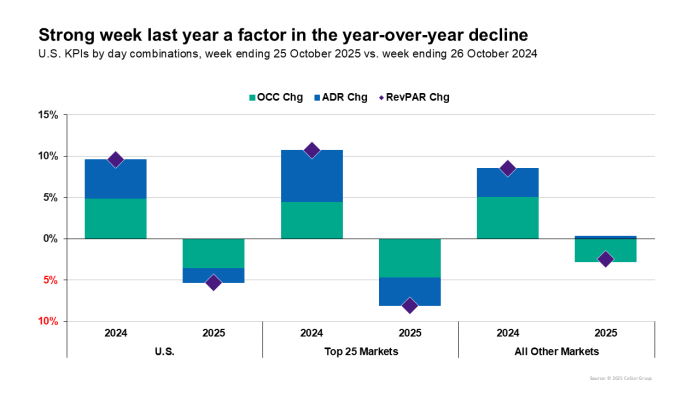

- U.S. RevPAR down against strong week last year

- Group demand falls for a second consecutive week

- 49% of U.S. properties down 5% or more

- D.C. down on government shutdown and conference shift

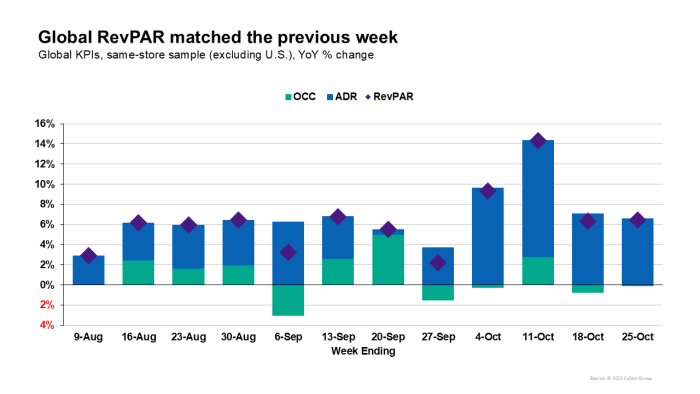

- Global growth continues

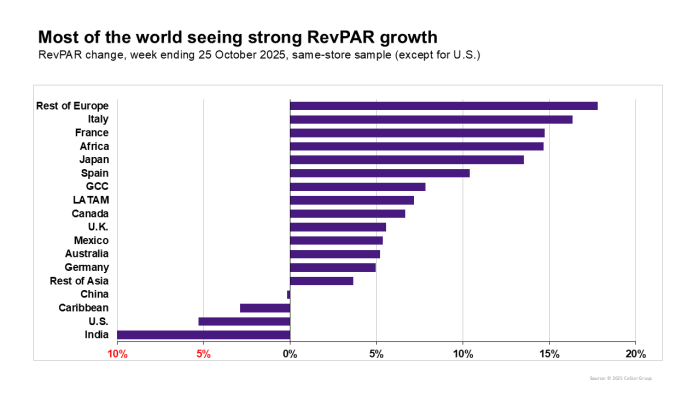

- Strong ADR-driven week for France

- India down during Diwali

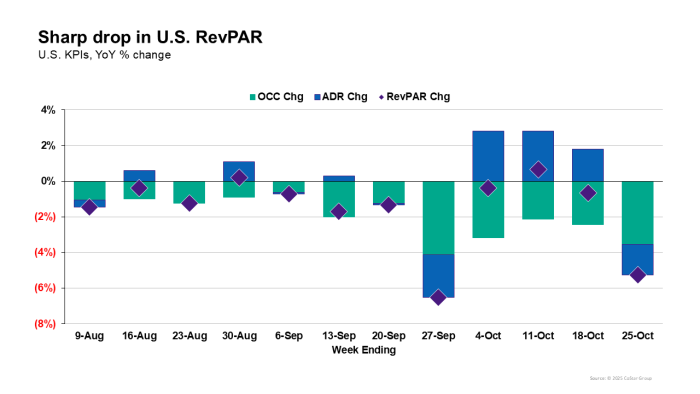

RevPAR falls sharply against strong comp

The week ending 25 October 2025 was a bad one for the U.S. hotel industry. Revenue per available room (RevPAR) dropped 5.3% year over year on falling average daily rate (ADR) and occupancy.