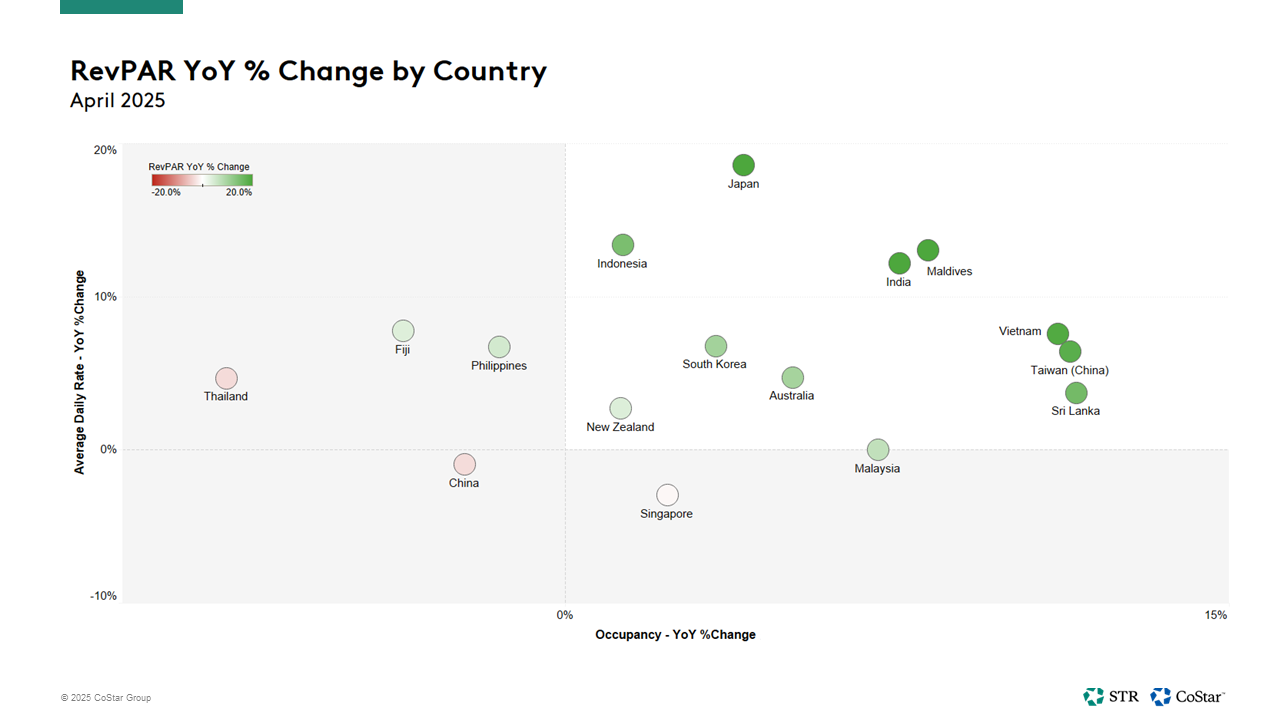

April performance across the Asia Pacific hotel industry was positive as 10 of the region’s 16 largest countries grew occupancy, average daily rate (ADR) and revenue per available room (RevPAR). In fact, all but three countries—China, Singapore and Thailand—experienced RevPAR gains.

The March/April period is often impacted by calendar shifts of religious events and public holidays. April 2025 was no exception with a shift in observances including Ramadan, Easter and Passover affecting both business and leisure travel patterns in the region.

Japan continues to hold the APAC region’s top spot

Japan remains the standout performer with seemingly unstoppable ADR gains. The country also advanced occupancy in April, which is the middle of Cherry Blossom season, a draw for visitors from around the world. April occupancy was Japan’s highest level in the past 12 months. A favorable yen-to-dollar exchange rate has contributed to Japan’s attractiveness for visitors, however the favorable FX rate is starting to subside. Expo 2025, held this year in Osaka, opened in mid-April and will benefit performance throughout the country until the middle of October.

Of the other Northeast Asian markets highlighted, Taiwan (China) and South Korea experienced occupancy and ADR increases. Similar to Japan, April is a popular month for both markets. In Taiwan, Taipei and Taiwan Regional lifted RevPAR with occupancy as the main driver. The Incheon & Seoul markets and Busan submarket drove performance for South Korea with generally equal parts occupancy and ADR.

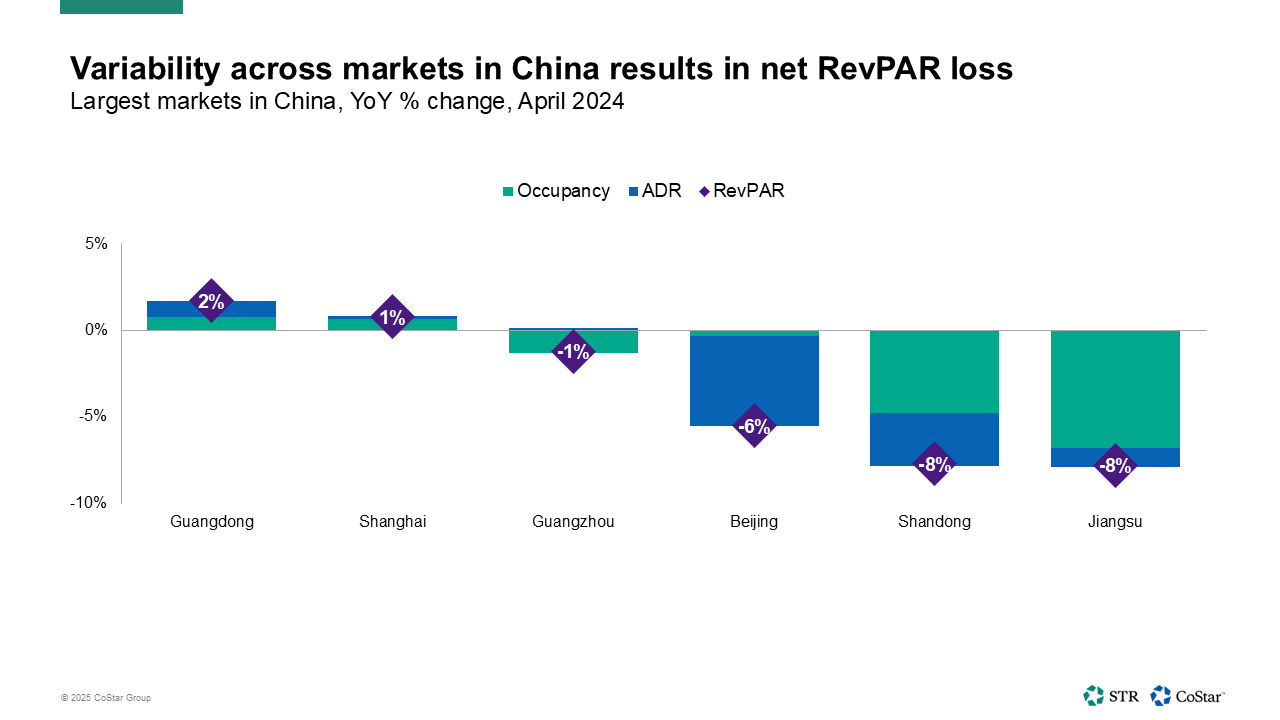

Variability across markets in China resulted in net negative performance

China, the largest country in the region, posted negative RevPAR comparisons impacted more by occupancy declines than ADR. Healthy supply increases have contributed to the country’s slowing occupancy. April performance varied across the country with Macau SAR and Sanya posting double-digit RevPAR increases, while the majority of markets posted declines. Similar variability was seen across the five largest markets where Guangdong and Shanghai experienced modest gains while Beijing decreased RevPAR due to ADR declines. Shandong and Jiangsu slowed primarily because of decreasing occupancy.

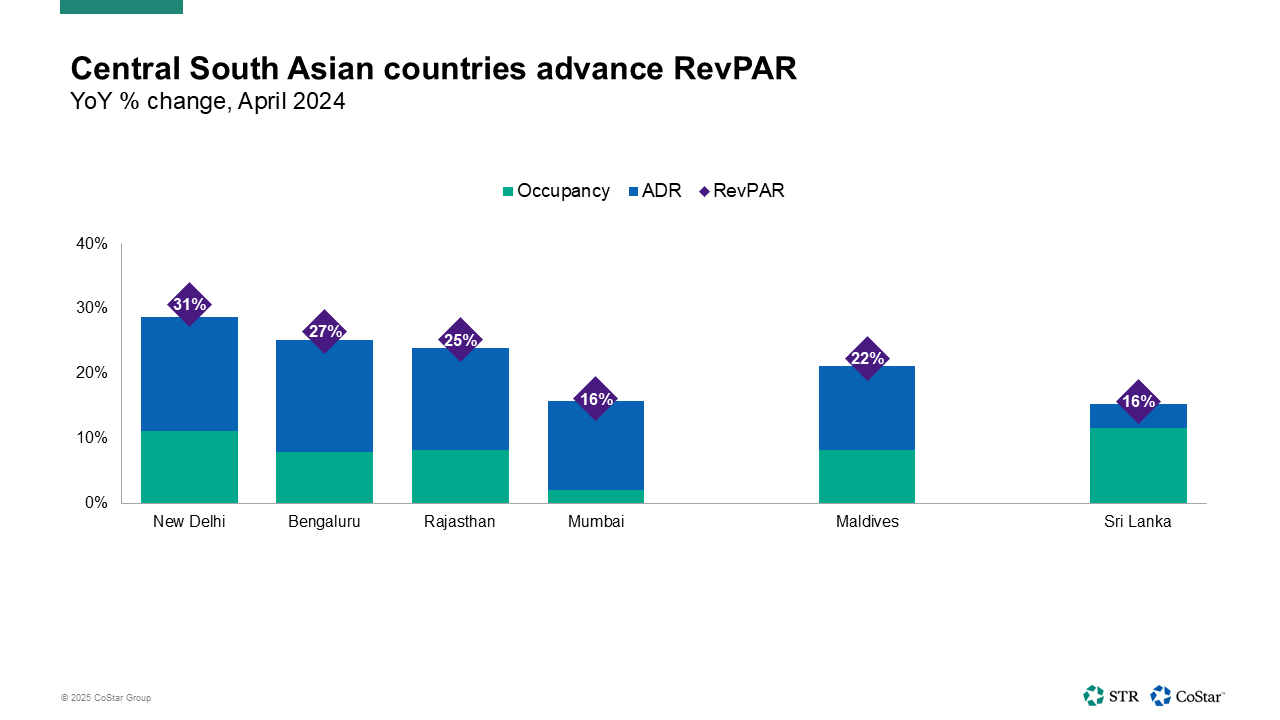

All three top Central South Asian countries advanced RevPAR

Three of the top countries in Central South Asia—India, Maldives and Sri Lanka—advanced RevPAR on both ADR and occupancy gains. India experienced growth throughout the country with the four largest markets posting double-digit RevPAR gains. Mumbai rose primarily due to ADR gains, while New Delhi, Bengaluru and Rajasthan saw occupancy and ADR increases. Highlighting the popularity of the country, all 17 markets in India experienced an occupancy increase in April.

Two smaller countries in the region—Maldives and Sri Lanka—increased RevPAR as well. Maldives, recording one of the highest ADRs in the region, has seen growth all year, while April was the first month this year that Sri Lanka posted positive performance.

Solid April performance in the southern hemisphere

April brought cooler weather and positive RevPAR comps in the southern hemisphere for the three highlighted countries in the region. Inflation, which has been a headwind in the region, has lessened.

FX rates are also a factor as the Australian dollar remains weak against the U.S. dollar, providing a tailwind to long-haul inbound travel. Australia’s top markets all posted healthy RevPAR gains, driven by occupancy and ADR. New South Wales, the third largest market in the country, achieved double-digit growth. New Zealand saw strong performance across all four submarkets in the South Island market. North Island was mixed with the two largest submarkets, North Island regional and Auckland, up and down, respectively.

Fiji experienced growth following a decline in March, in part because of the Easter/Passover calendar shift which benefits leisure travel, providing a boost to a vacation market such as Fiji.

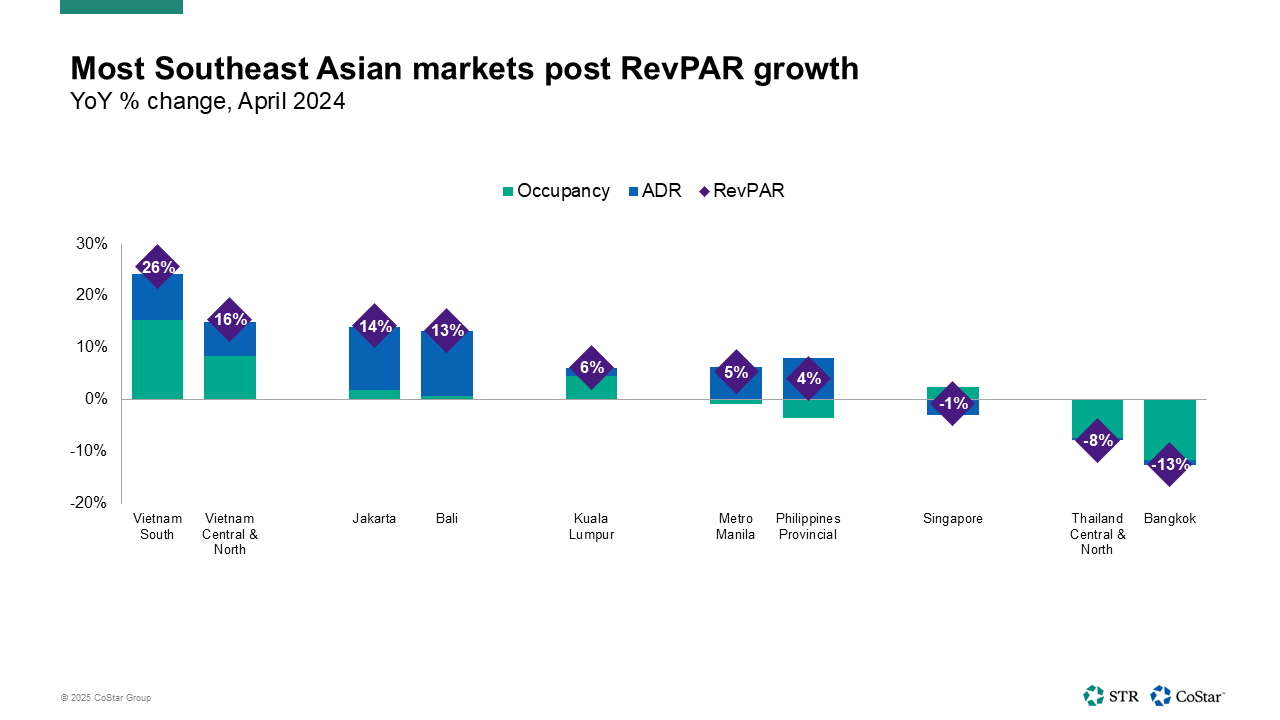

Variable performance seen across Southeast Asia

Performance was mixed across Southeast Asia. Vietnam and Indonesia recorded RevPAR gains via increased ADR and occupancy. In Vietnam, all seven submarkets increased RevPAR. April in Indonesia was positive following negative performance in March, impacted by above mentioned calendar shifts. Two of the largest markets, Jakarta and Bali, each produced double-digit gains driven almost entirely by ADR.

Occupancy was the exclusive driver of positive RevPAR performance in Malaysia and Singapore. Both countries recorded stronger performance in April compared to March with Malaysia netting positive KPIs while Singapore retreated slightly. Singapore consistently posted the highest occupancy and ADR of any country in the region.

Occupancy declines suppressed RevPAR in the Philippines and Thailand. Increasing ADR in the Philippines made up for the occupancy decline both in Manila and the surrounding region. Performance was mixed across Thailand, with Bangkok and Thailand Central & North seeing modest ADR declines and more significant occupancy declines. Phuket and Thailand South posted positive RevPAR with ADR being the primary driver.