As countries across Europe begin to surface from lockdown, new trends in hotel performance have emerged as a result of the COVID-19 pandemic. Recent data suggests a distinct preference for regional destinations or, “coast and country,” as STR Director of Account Management Aoife Roche explained in a recent webinar.

Beach bums

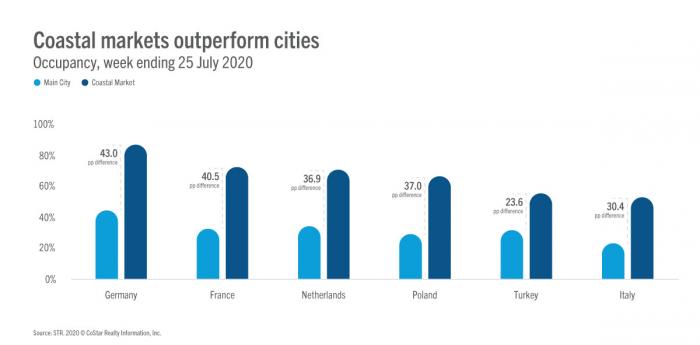

Coastal occupancy was on average 35 percentage points higher than main city occupancy across six European countries for the week ending 25 July 2020. Even Italy, once the epicenter of COVID-19 in Europe, reported 53% occupancy in the Basilicata/Calabria/Puglia market.