A key question in the hospitality industry is just how long will hotel bookings be affected by the COVID-19 pandemic? In short, while there is no simple answer, our occupancy-on-the-books data provides invaluable insights into the current trend of declining future demand.

The travel restrictions, lockdown measures, and severity of the COVID-19 pandemic were mirrored by declines in hotel occupancy on the books as March progressed. At first, there was a slowdown in bookings before cancellations began to come through for the short-term and were eventually outpaced by a declining number of bookings. The escalation of the pandemic has meant that, what was once an issue for the following 14 or 28 days from a March date, extended into the summer months to varying degrees in key markets.

How far does that trend extend into 2020?

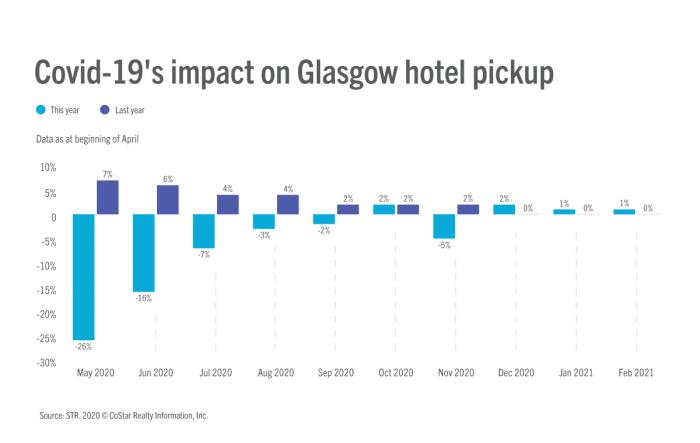

To get a feel for the impact of COVID-19 across the end of 2020 and into early 2021, we’ve focussed on three markets in which we have occupancy-on-the books data for the same time last year: Edinburgh, Glasgow and Zurich. Our data is taken from our latest 365 forward data report, produced on 6 April.

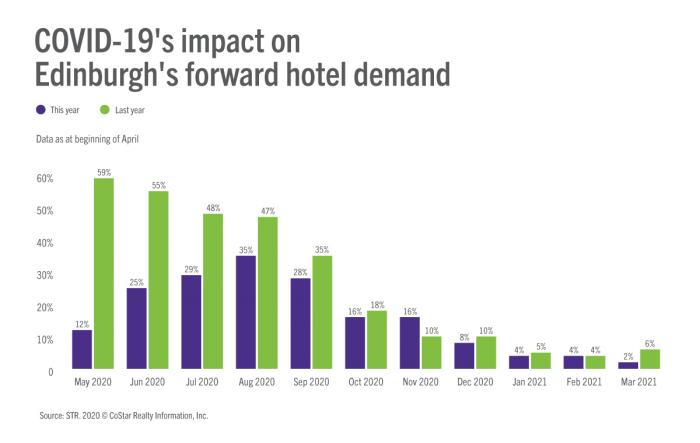

Edinburgh

In the short-term, we can see that the market is much further behind where it was at the same point last year. It is not all doom and gloom, however, as in November, the market is pacing ahead of where it was last year—with 16% occupancy on the books overall compared to 10% in 2019. Although, as we have seen for so many Forward STAR markets, cancellations continue to come in for the immediate future, while the second half of the year remains relatively unaffected.