Analysis by Kelsey Fenerty

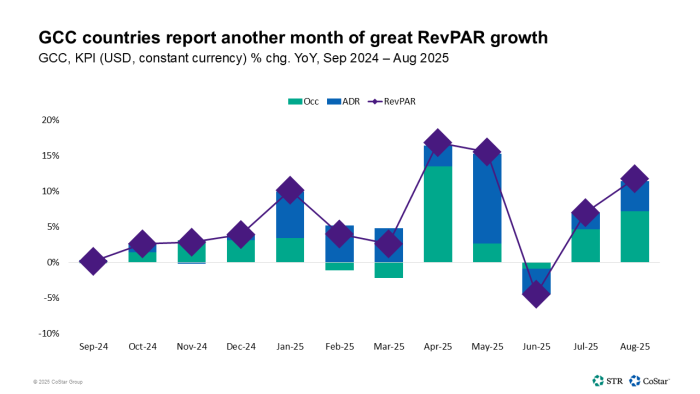

Despite the summer heat, hotel performance has accelerated across the six Gulf Cooperation Council countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates).

In August, revenue per available room (RevPAR) grew 11.7% year over year with gains in both occupancy and average daily rate (ADR).