As markets slowly begin to reopen and leisure demand picks up, specifically on weekends, it is important to look towards business-on-the-books data to see how these markets will perform in the coming weeks and months.

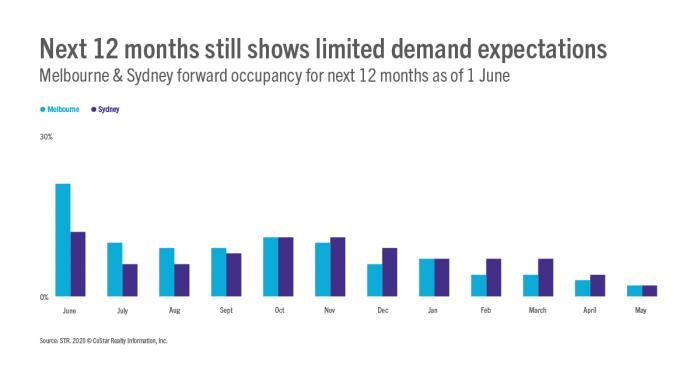

While evaluating past data is crucial for the industry, it is imperative to take a step into the future to see how your hotel may compare against your market or competitive set. STR’s Forward STAR reports do just that—look 90 or 365 days ahead with this report to strategize more efficiently by correlating uptake in bookings with your marketing and promotional campaigns, as well as events or conferences in your area.

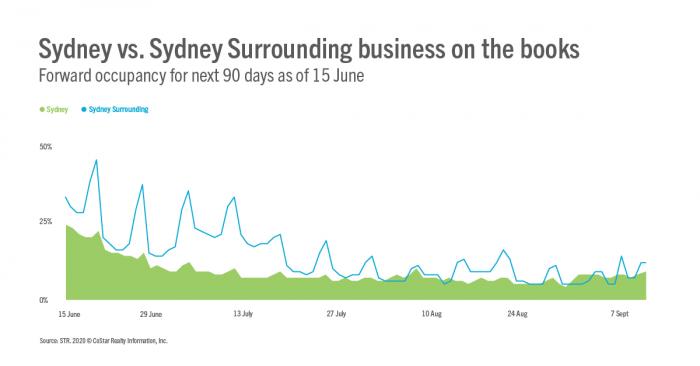

STR currently has forward demand data for five markets across Australia: Sydney, Melbourne, Sydney Surrounding, Adelaide and Darwin. This is only the beginning of our forward-looking data, as we are continually working to add new markets.

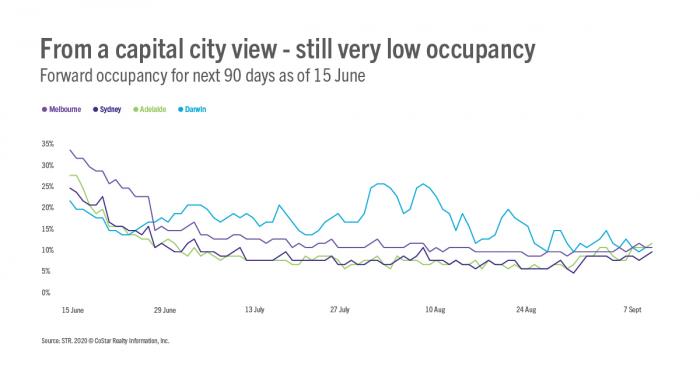

The next 90 days

As of 15 June, when looking at the next 90 days (through 7 September), there is still very little forward occupancy across the four capital cities and the Sydney Surrounding area.

Among the four capital cities, forward occupancy sits below 20% in all markets except Darwin, which shows occupancy above 20% between 27 July and 10 August.