With global travel trends shaped by a mix of factors, the upcoming months feel more unpredictable when it comes to traveler confidence and the impact on hotel performance. With the potential for lower international inbound arrivals emerging as a key concern, STR conducted a projection to assess the possible impact on U.S. hotel demand.

The likeliest scenario would create a limited impact

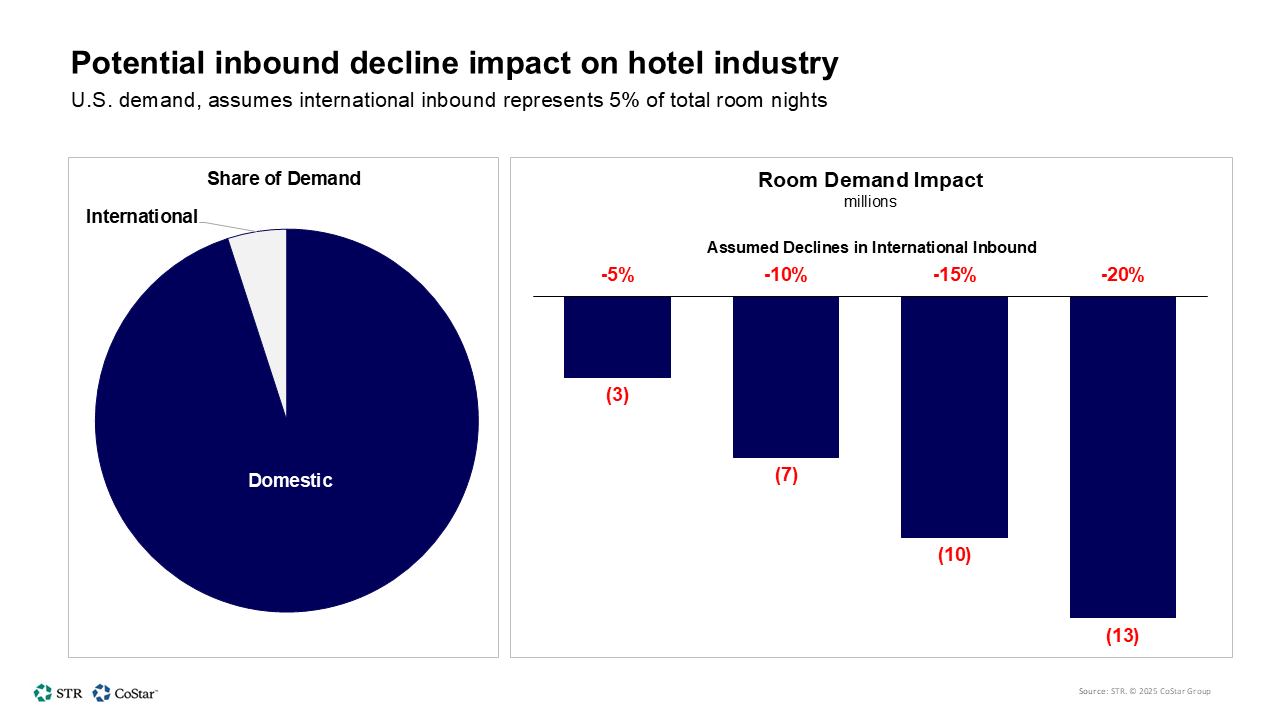

Tourism Economics estimates that international inbound arrivals account for 4-7% of total U.S. hotel demand, measured in room nights. Based on recent shocks to the economy, as well as an 11.6% drop in overseas visitor arrivals in March, Tourism Economics is projecting a 9% decline in international inbound arrivals for 2025 (-20% from Canada).

Using the January 2025 forecast, STR ran four scenarios to show the potential impact on U.S. hotel demand. If international inbound falls 5% for the year, the industry would lose 3 million room nights sold. For context, U.S. hotels sold 1.3 billion room nights last year.

Of course, if the decline in international inbound is steeper, the impact on demand becomes more significant. Our analysis shows that a 1% reduction in international inbound would reduce hotel demand by 654,000 rooms on an annualized basis.

Recent performance

Q1 2025 included several major demand influencers that impacted the industry. Three were built into the calendar – the presidential inauguration in January; Super Bowl shift from the largest U.S. hotel market (Las Vegas) in 2024 to the 38th largest market (New Orleans) in 2025; and the College Football Playoff Championship shift from Houston (2024) to Atlanta (2025). Two were not built into the calendar—the Los Angeles wildfires and continued impact from the fall 2024 hurricanes.

Those demand influencers, along with a later Easter, made for a messy calendar when analyzing potential performance impacts from the geopolitical environment.

March rounded out Q1 with a whisper following two stronger months. RevPAR increased a modest 0.8% in March following gains of 2.1% and 4.3% in February and January, respectively.

RevPAR for the quarter advanced 2.2%, and ADR was the primary driver of that growth all three months. Among day types, weekdays produced the largest increases in occupancy and ADR.

April preliminary data through the 26th showed expected fluctuations, mostly negative, given the Total Eclipse comp from last year then the Easter and Passover holidays. Easter week demand, specifically, was higher than the holiday week the last two years. Overall, for 1-26 April, RevPAR was down 0.3% YoY on a 2.1% drop in occupancy. U.S. weekend occupancy (for the week ending 26 April) climbed to 77.3%, marking the highest level since the weekend of 18-19 October 2024, when it reached 78.3%. For context, in 2024, weekend occupancy didn’t exceed 77% until mid-June and only surpassed that threshold six times throughout the entire year.

Demand in U.S. hotels within proximity to the Canada and Mexico borders has wavered the last two months with no conclusive evidence of a trend.

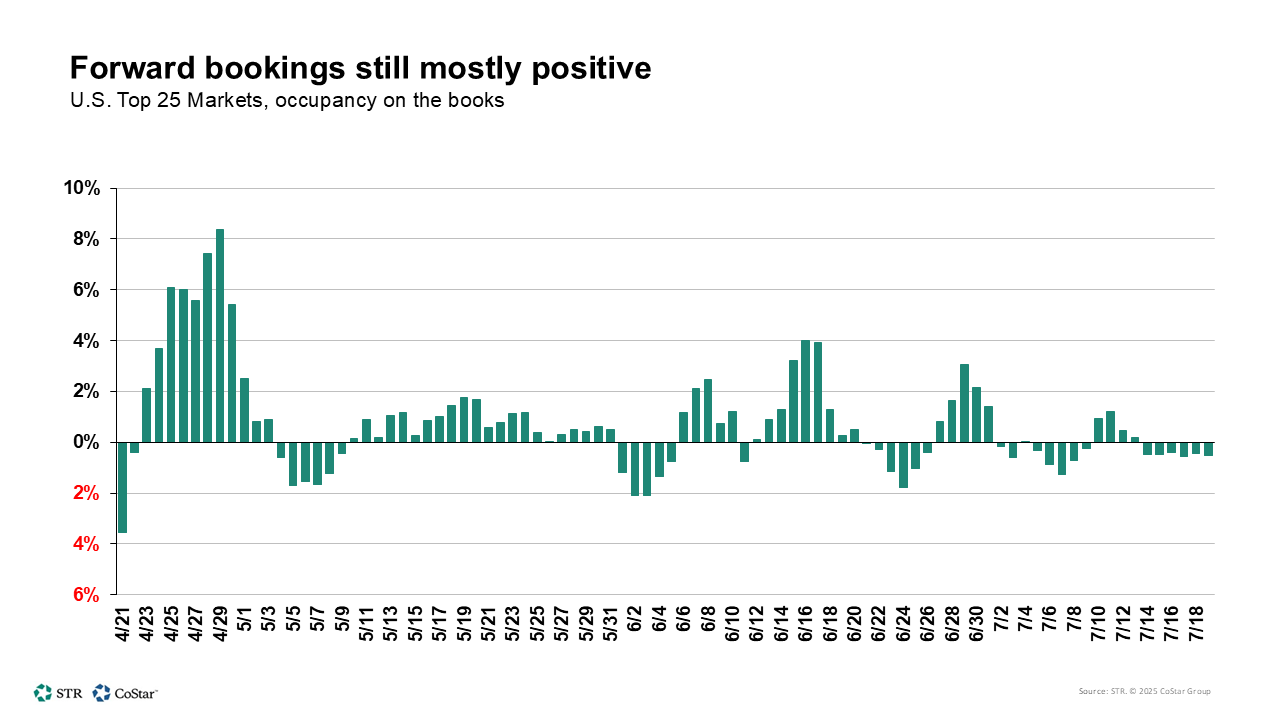

Future bookings

Forward bookings among major U.S. markets in aggregate look mostly steady for the coming months. Of course, the story is not the same in every market. For example, D.C. is down around 3 percentage points on average through June, while San Diego is up around 6 ppts.

Other metrics/indicators we are watching

- ADR growth has been the primary driver of RevPAR in our forecasts this year. However, it will be important to monitor for any slowdown to gauge if properties are discounting rates to gain market share.

- There has been some discussion about potential softening in long-term Group bookings. This could reflect shorter booking windows as planners wait for more market certainty, or it could signal a longer-term decline. Group demand has been resilient in recent years, so any sustained downturn would warrant a reevaluation of the overall demand outlook.

- TSA screenings were up the past three weeks, which aligns with the holiday and spring break travel. In the week ending 26 April, screenings grew 2.7% YoY.

- As shown by data from the U.S. Department of Labor, layoffs have remained mostly stable, and new unemployment claims have seen a slight rise since last year.

- According to the Bureau of Economic Analysis, consumer spending held in Q1 with 3.1% YoY growth.

Looking ahead

In a recent episode of Tell Me More: A Hospitality Data Podcast, STR’s Isaac Collazo and CoStar Group’s Jan Freitag cautioned the industry to avoid recency bias and overreactions in their decision-making. The data has been noisy, as expected, and there are a lot of conflicting signals in the market.

The key is to trust the data and lean on complete analysis. The calendar will be cleaner for year-over-year comps moving forward, so that part of the process should be less tricky to navigate.

A revised forecast from STR and Tourism Economics will be released during NYU IHIF in early June.