Did you miss one of our webinars? Don’t have time to watch the full recording? No problem. We are pleased to present the key points in this latest COVID-19 webinar summary. In this edition, we talk performance in the Middle East and Africa.

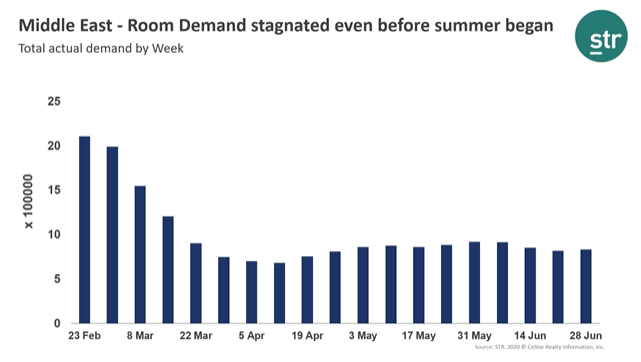

Middle East demand stagnated even before summer began

For the week ending 28 June, over 834,000 rooms were occupied across the Middle East, an average of 119,000 rooms a day. On 23 February, before COVID-19 pandemic, 300,000 rooms a day were occupied in the region.