Website update in December We’re pleased to announce a streamlined customer journey with the integration of str.com into costar.com. Beginning in early December, any visit to str.com will be rerouted to costar.com. To enter property data or access the STR Client Site, log in here or via the Benchmark page of costar.com. More details here. Learn More.

Central/South America’s hotel pipeline is weak, but a handful of markets project significant growth

Share

7 July 2021

Data Insights Blog

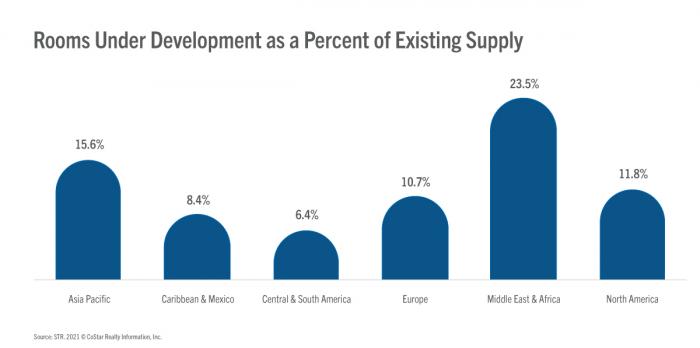

Hotel development in the Central and South America region is lagging noticeably behind the rest of the world with just 39,000 rooms in the planning, final planning and in construction phases combined. Overall, the region’s hotel pipeline accounts for just 6.4% of existing supply, which is less than half the rate of global hotel development at 12.9%.

Image

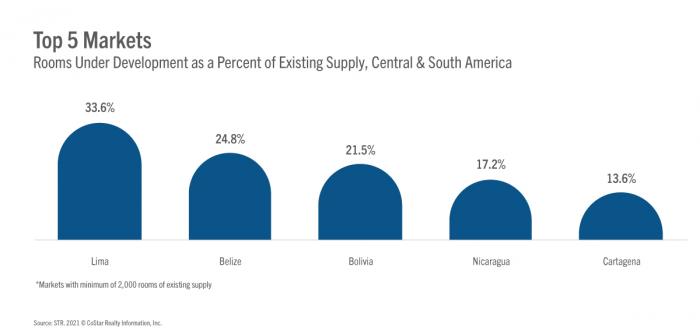

Despite the collective, sluggish pipeline activity in Central and South America, there are five markets which are experiencing spurts of significant growth above the global average.

Here is a quick overview of a few of the region’s hotel development hotspots when ranked by projected supply growth.

Lima projects as the fastest growing market in the region with more than 4,100 rooms under development, a number that would produce a 33.6% supply increase in the market if all those rooms are completed. More than half of the rooms in the pipeline are upscale class or above. The capital city has experienced significant economic growth in recent years, and Peru is maintaining its 10% GDP growth projection this year, which would represent the fastest rate on the books since at least 1994.

The country of Belize—a market in and of itself—will see its hotel supply grow by nearly 25% if all projects under development are completed. Nearly half of the development activity is concentrated in the resort area of San Pedro, in northern Belize, famous for its sandy streets, cuisine and coral reefs.

Bolivia, the landlocked nation in the central portion of South America, is projected to increase its hotel supply by 21.5% upon completion of all projects. Among the eight projects underway, five are in Santa Cruz, the nation’s commercial hub, which has seen significant growth in recent years and has evolved into a modern, cosmopolitan center.

Nicaragua, the largest country on the isthmus of Panama, has the fourth highest rate of projected hotel growth in the region with rooms under development accounting for 17.2% of existing supply. Five of the six projects underway are in Managua, the capital city.

Finally, Cartagena, the port city on Colombia’s Caribbean coast, clocks in with the fifth highest projected growth rate of 13.6%, which covers 11 projects. Six of those projects are in the coastal, resort areas of the market.

Image

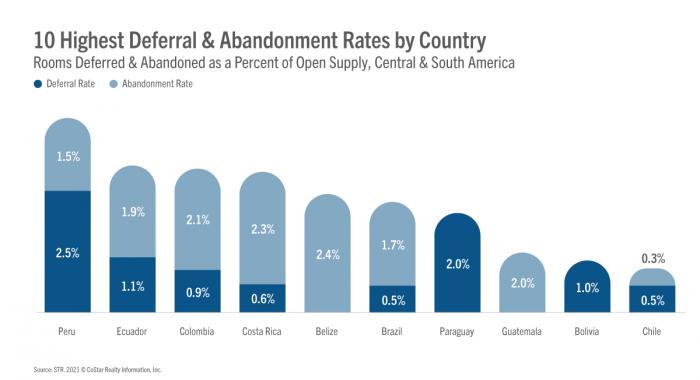

While these markets stand out as high-growth examples, the number of deferred and abandoned projects in the region symbolizes the economic struggles that have worsened throughout the pandemic period. For instance, in Brazil alone, more than 30 projects (or nearly 5,000 rooms) have been abandoned in the past 12 months, while another 10 have been deferred for development until a later date.

With Peru and Ecuador leading the way, many countries and markets in the Central and South America region have above-average rates of deferred and abandoned projects. Still, the region’s average of 2.0% of projects deferred/abandoned is marginally lower than the global rate of 2.33%.

Image

For further insights into COVID-19’s impact on global hotel performance, visit our content hub.