While the health and wellbeing of so many around the world is the primary focus right now, we also want to do our best to support our partners and answer as many questions as we can around performance and data reporting. We want to extend our gratitude to all hotel partners for continuing to provide accurate and timely data per STR reporting guidelines. This is key as we monitor and report during this abnormal period, and eventually forecast market recovery.

Latest data on Mainland China

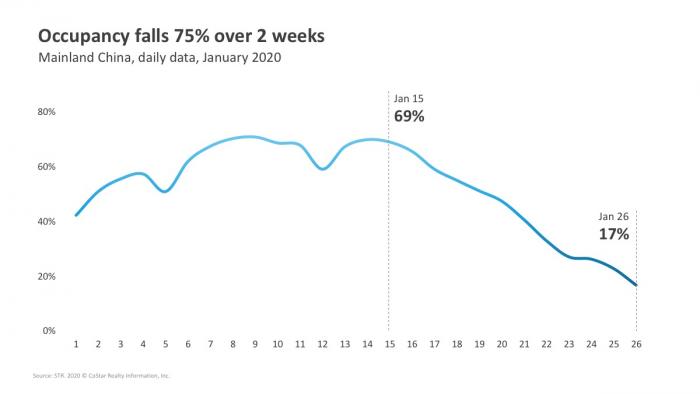

STR analyzed historical data as well as preliminary daily data for the first 26 days of January. It was important to consider the combination of Chinese New Year in addition to the coronavirus outbreak.

- The Chinese New Year holiday week, extended by three days in 2020 to 2 February, normally produces a significant shift in travel patterns across the country with very specific hotel occupancy movements. This is due to less business travel, school closings and those who return home to spend their holiday with family. At the same time, it is normal to see average daily rate (ADR) rise to levels higher than the yearly average in the market.

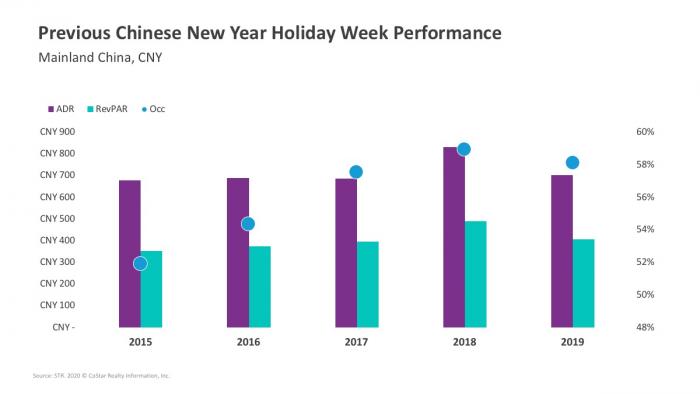

- With that trend in mind, Mainland China’s occupancy reached 70% on 14 January but proceeded to fall to a lower absolute level each day thereafter. In the final day of our analysis (26 January), occupancy had dropped to just 17.0%, representing a 75% decline from the 14th of the month. ADR began to ascend on 19 January, eventually reaching a monthly high of CNY754.48 on 26 January, which represented a 61% increase from the 19th of the month.