Knowing you might not have time to watch our full webinars, we are pleased to continue our series of COVID-19 webinar summaries. In this latest edition, we talk performance in Asia Pacific.

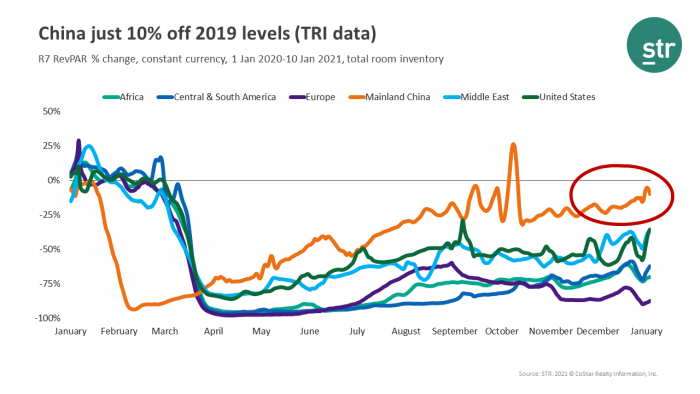

Mainland China just 10% off its pace

When using total-room-inventory (TRI) methodology, which excludes temporary closures due to the pandemic, Mainland China RevPAR was just 10% behind its 2019 RevPAR levels. This was well ahead of other key regions around the world.