Analysis by Brannan Doyle

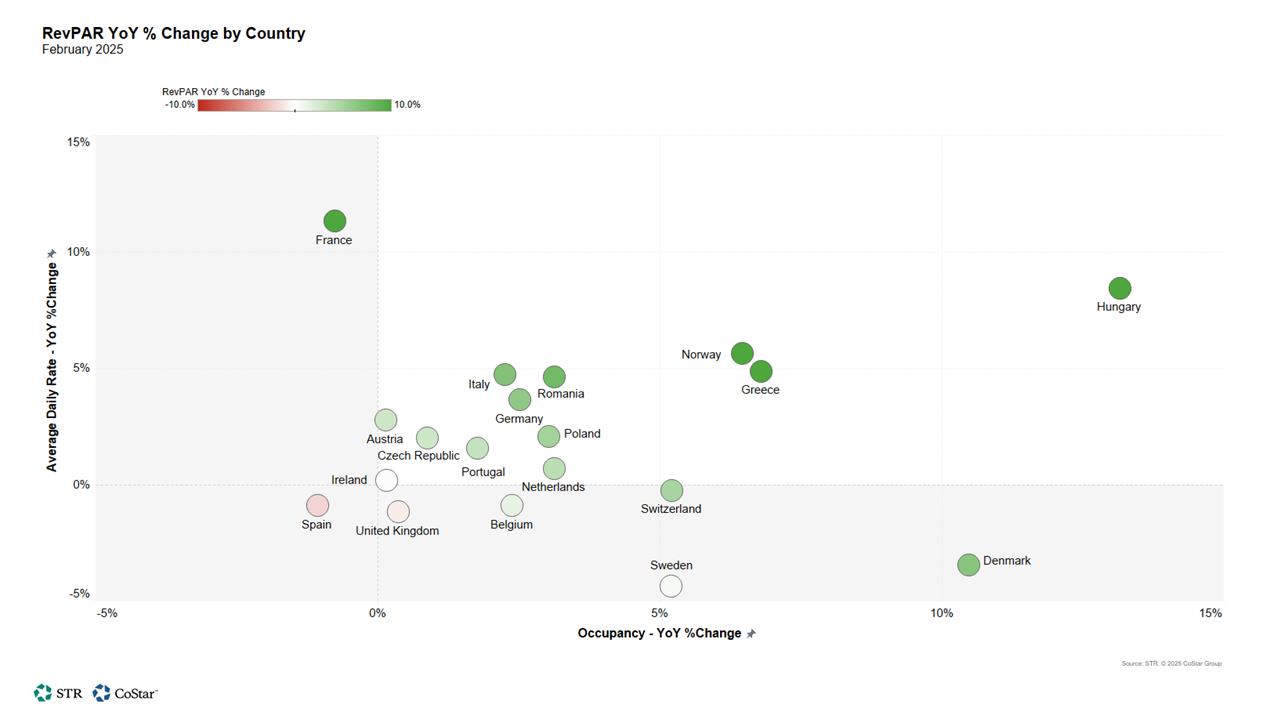

Most major European markets saw year-over-year (YoY) performance growth in February 2025, ranging from subdued to substantial. In some countries – France being a notable example –revenue per available room (RevPAR) grew YoY for all major markets. Elsewhere, countries saw gains in some markets offset by sluggish performance in others.

In plotting RevPAR growth by occupancy contribution versus rate contribution, a few noticeable trends emerge. The RevPAR lift in France was driven entirely by hoteliers’ pricing power, even at the expense of a modest dip in occupancy compared to February 2024. In Denmark, the opposite was true – occupancy grew roughly six percentage points (thanks to a more than a 10% increase in demand), while average daily rate (ADR) slid downward 3.5%. Turkey is intentionally omitted from the chart below, with a greater than 20% increase in room rates for February driven chiefly by inflation.

Hungary led in RevPAR growth with sizable contributions from both rate and occupancy. There’s likely a combination of factors at play here; occupancy in Hungary for February 2024 was unusually low compared to 2023, making the upward trend in 2025 more pronounced. And with many markets in western Europe experiencing overtourism and an increase in compressed room nights, travelers from overseas may be pushing deeper into Europe seeking more affordable rates and convenient accommodations.

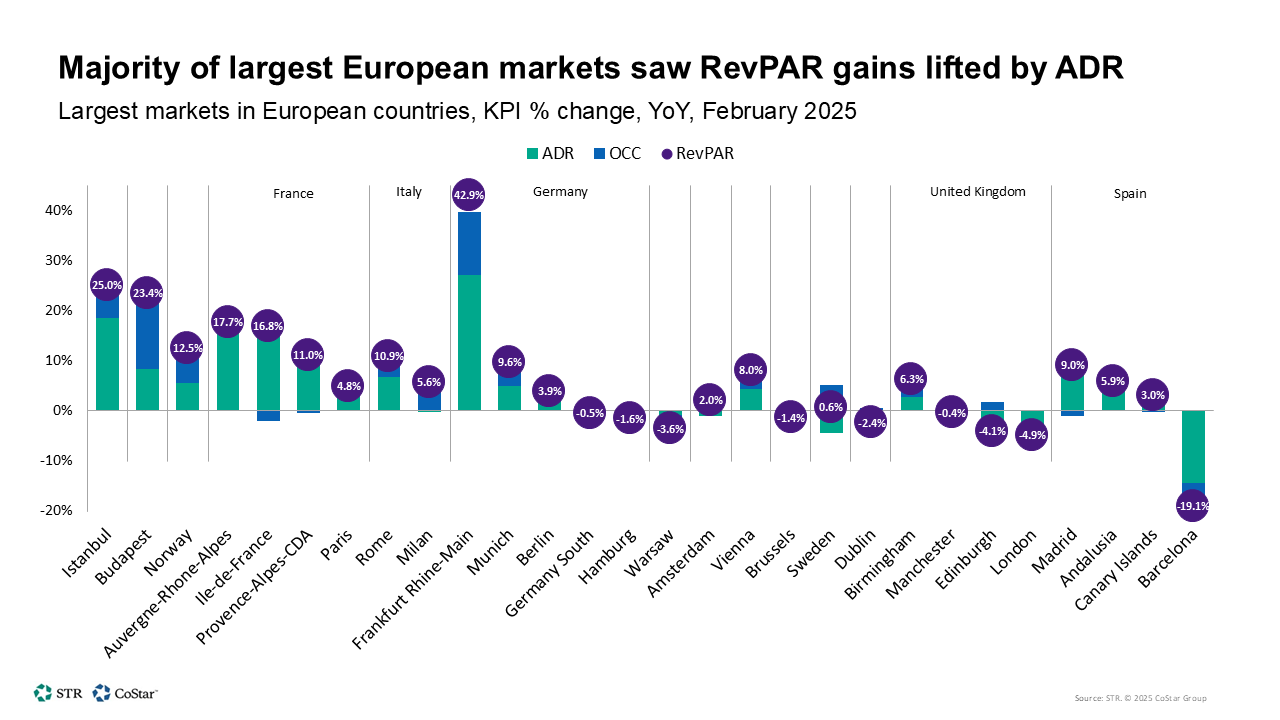

When scanning Europe’s major markets, Frankfurt’s February performance dominated the field. Ambiente, a major trade show for consumer goods, shifted from late January in 2024 to mid-February in 2025 — lifting both occupancy and pricing power for the month. French markets continue to push rates, resulting in RevPAR gains across the country, even exceeding +15% in some markets. A couple of Italy’s major markets saw consistent RevPAR increases as well, with Rome gains driven mainly by rate growth and Milan boosting occupancy by a healthy margin.

In Spain, most markets saw healthy RevPAR gains, with Barcelona being the notable exception. The shift of the Mobile World Congress from late-February to early-March was a damper on February’s metrics for Barcelona and for the entire country. Spain’s March performance will reveal the offset.

Istanbul’s RevPAR growth of 25% was rate-driven and had a significant impact on Turkey’s overall performance. It is fair to attribute much of this growth to the inflation seen across Turkey.

In Hungary, the trajectory in Budapest, however, is more weighted toward occupancy gains year over year. With HUNGEXPO bringing a number of mid-sized trade fairs to Budapest each February, this could be a trend attributable to increased commercial demand in the nation’s capital, which we’ll be eager to follow as the high season of large conferences and expos draws near.

Check back next month for a dive into performance across the MEA region.