Every industry experiences change, growth and evolution over time, and the tourism and hospitality sectors are no exception. With this in mind, we take a closer look at how American hotel supply has developed over time—not just by number of new properties and rooms but through the evolution of the different hotel ownership models.

American hotel supply (2000-19)—room for growth, literally

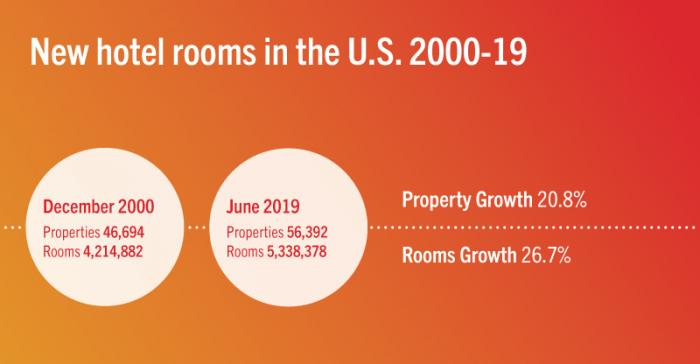

Close to 10,000 additional properties have entered the U.S. hotel industry over this nearly 20-year period, resulting in an inventory increase in excess of 1.1 million rooms. Digging a little deeper, 2008 and 2009 produced the largest year-over-year new supply increases of 3.0% and 2.6%, respectively, before five years of sub-1% growth. If those five years were a little underwhelming, the following five since 2015 (including June YTD 2019) welcomed increases exceeding 1%, with incremental yearly lifts that included a 2.3% jump in new rooms during the opening half of 2019. That gain in new supply for the first half of this year was highest for that period since 2009.