This research article analyzes previous crises across key countries in the Asia Pacific region to understand the impact on hotel profitability. While COVID-19 has presented unprecedented challenges for the global hotel industry, looking back at past situations shows the industry’s ability to recover.

STR’s research revolved around seven major countries in the region: Australia, China, Indonesia, Japan, Malaysia, Singapore and Thailand. These countries provide the strongest and most consistent P&L sample from 2002 through 2019.

*All financial figures represent US$ constant currency.

Different crisis, different impact

- The SARS outbreak lasted roughly six months and spread to more than two dozen countries before being stopped in July 2003. Data from Oxford Economics does not show any major impact on GDP growth due to the shorter time of the outbreak and less reliance on international demand compared with today. However, Australia was the only country that maintained hotel revenue and profit growth. Annual P&L data (excluding Australia) shows that the region’s occupancy fell 10.9%, while average daily rate was down just 1%. Gross operating profit per available room (GOPPAR) declined 1.5 times more than total revenue per available room (TRevPAR).

- The Indian Ocean Earthquake and tsunami of 2004 severely affected 14 countries as one of the deadliest natural disaster in history. Regardless, there seemed to be no impact over annual economic data from Oxford Economics, and hotel data showed only a slight occupancy decline, driven mostly by Phuket and the Thailand South markets (leisure destinations) during the impacted month. There was no visible impact on annual performance.

- The Japan Tsunami of 2011 was one of the worst natural disasters in the country’s history and stifled GDP, which declined 0.1% from the previous year. However, hotel data does not show a major impact with only a 2% drop in GOPPAR, mostly a result of 4% decrease in occupancy.

- The 2014 Hong Kong protests lasted more than two months and led to a double-digit decline in hotel ADR (-11.3%) even as occupancy remained steady during that time. There also was no impact on GDP growth. A lagged effect on demand was visible in 2015 when we saw the number of rooms sold in the market fall 1.6%. Hotel profitability data showed a similar trend with no impact in 2014 but a 9.3% drop in GOPPAR in 2015. Recovery did not occur in full until 2017.

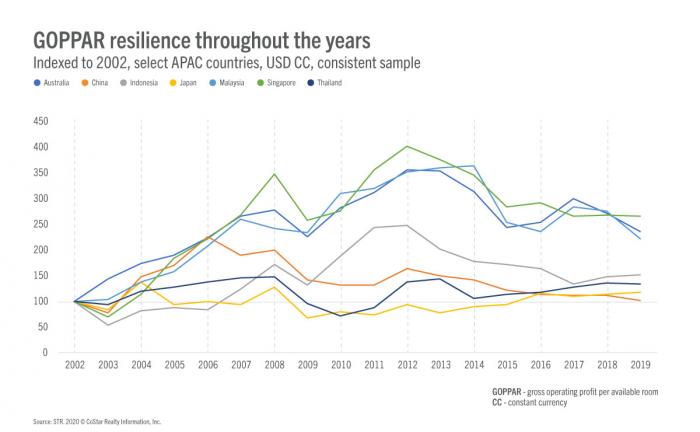

- The Global Financial Crisis of 2008-09 started in the U.S. but spread around the world. This is the only crisis where we see an impact across all seven countries in our analysis, as clearly demonstrated by the graph below.