India hotels achieved a 50% occupancy level in February, which was the first time the country eclipsed that monthly mark since the start of the pandemic.

Occupancy climbed to 54.5% (-23.5% year over year), while average daily rate (ADR) reached INR4,361.46, a drop of 31.4% year over year. The ADR level was the second highest since the start of the pandemic, trailing behind December 2020 (INR4,554.29).

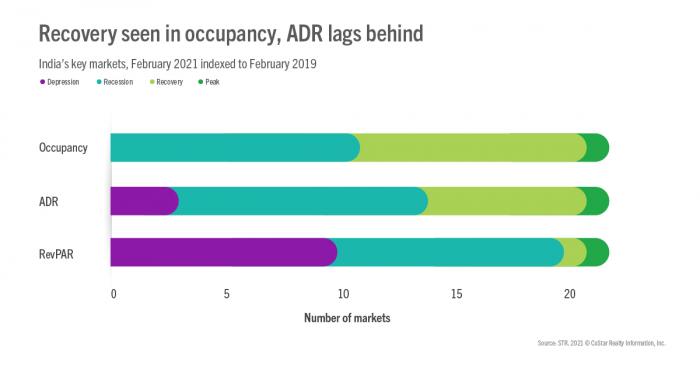

While the actual levels are something to cheer about, the year-over-year percentage changes have become less actionable when analyzing performance recovery. STR’s new Market Recovery Monitor compares the performance of key markets within the country to the same month in 2019, considered the pre-pandemic “normal.”

This model represented below, places markets into four recovery buckets, based on their indices to the same month in 2019 for occupancy, ADR and revenue per available room (RevPAR).

The indices are calculated by dividing the market’s current performance against performance in the same month in 2019.

The recovery buckets are:

- Depression: Markets with an index of 50 or below against the benchmark

- Recession: Markets with an index of between 50 and 79.9

- Recovery: Markets with an index of between 80 and 99.9

- Peak: Markets with an index of 100 or higher.

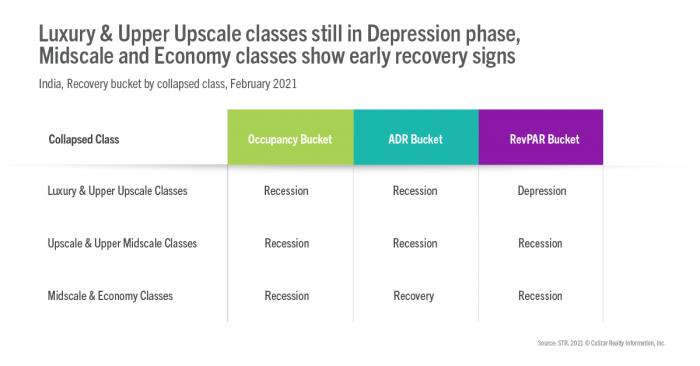

At a collapsed-class level for RevPAR, Luxury & Upper Upscale classes remain in the Depression phase, whereas the Upscale & Upper Midscale classes and Midscale & Economy classes are in the Recession phase.

ADR for the Midscale and Economy classes shows early signs of recovery.