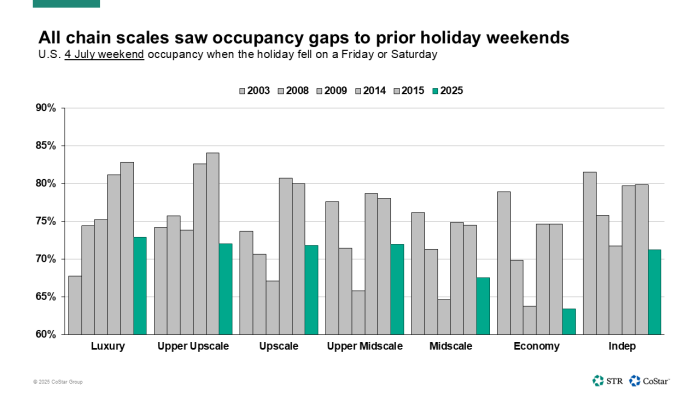

The Fourth of July holiday has long served as a key indicator of leisure travel and lodging demand in the U.S. Amid ongoing macroeconomic pressures and weakening hotel performance metrics, this year’s holiday weekend faced heightened scrutiny. Fortunately, the holiday passed the test when it came to hotel demand.

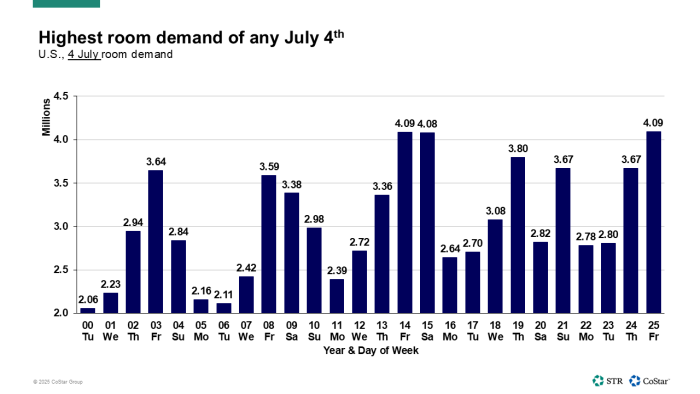

Record-high July 4 room demand

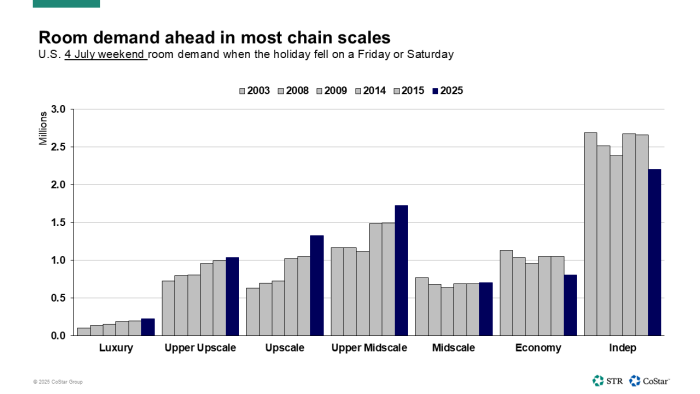

For just the second time since daily reporting began in 2000, the U.S. hotel industry topped 4 million rooms sold on July 4.

At 4,092,239 room nights, this year topped 2014 (also a Friday) and 2015 (a Saturday) by more than 3,000-plus rooms.