Are you tracking the Market Recovery Monitor each week? Utilizing data and benchmarking to navigate recovery will be a key focus of the 2021 Hotel Data Conference. Click here for registration, with both in-person and virtual options available for our 13th annual event in Nashville.

Previous MRM version: 26 June | 3 July

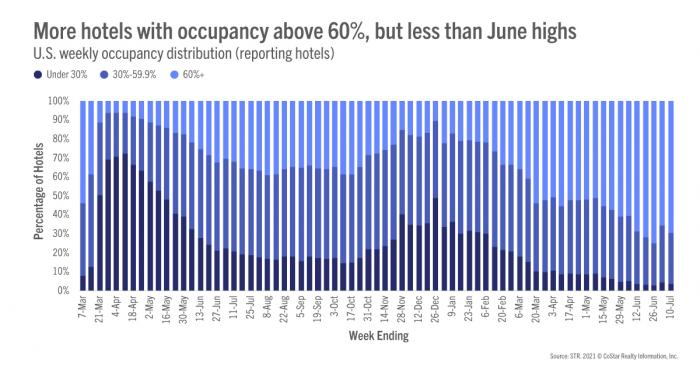

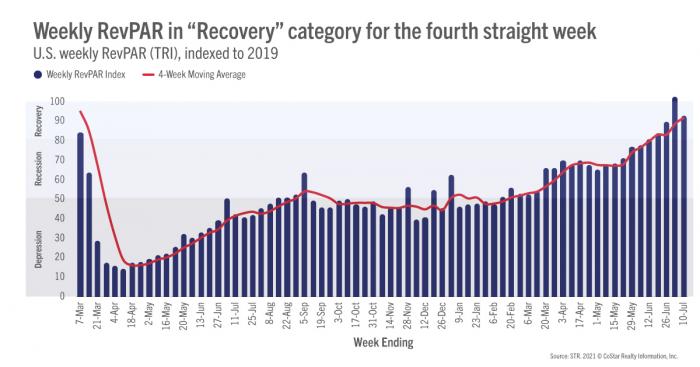

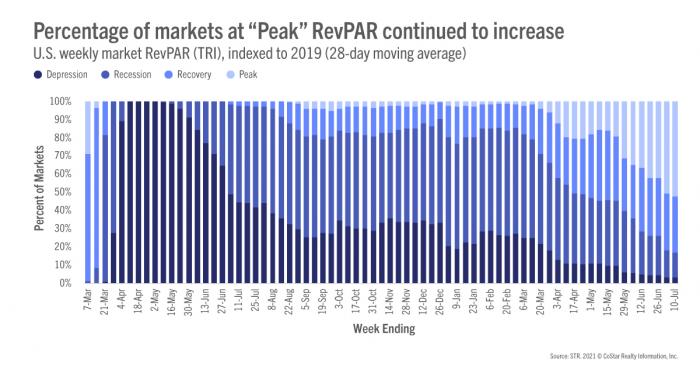

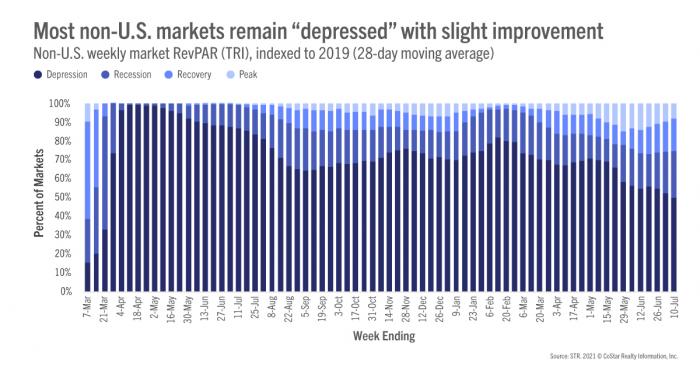

Week ending 10 July

Following the normal pre-4th of July slump, U.S. industry occupancy rebounded to 67.2% for the week ending 10 July 2021. While this was good news, the gain was much less than expected as weekly demand improved 3% to 26 million. In the same week of 2019, demand increased 13% week over week, and occupancy hit 74%. We believe this illustrates the continued shortfall in business and group demand that in normal times would have supplemented seasonal leisure demand. Daily occupancy peaked again on Saturday at 80%, which was the fourth time this year that Saturday’s occupancy was above 80%. Sunday, 4 July occupancy (66%) was solid but not as strong as on Memorial Day Sunday (68%). Despite the higher Sunday occupancy, weekday occupancy was virtually unchanged from the previous week (+0.2 points) and 2.6 points lower from its high three weeks ago. On a total-room-inventory basis (TRI), which accounts for temporarily closed hotels, weekly occupancy was 64.7%.