Spring Break 2021 didn’t just dive in, it made a cannonball-sized splash for Florida hotels and other U.S. destinations.

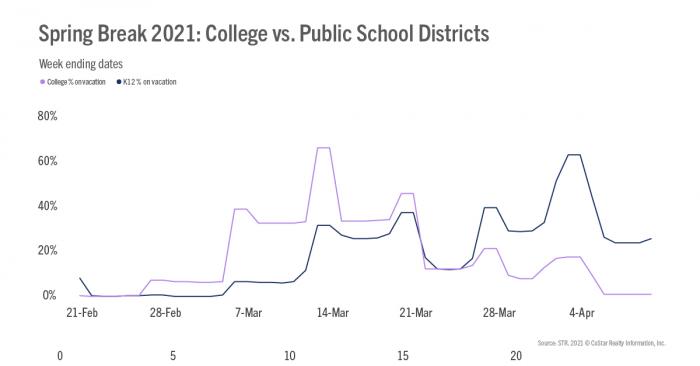

When looking at STR’s School Break Report, 39% of college students and just 7% of K-12 students were on break beginning 6 March. Despite this slightly low percentage, all signs pointed to a strong spring break period right out of the gate. The STR-defined Florida Keys market, at that point, was the only U.S. market to reach an 80% occupancy level—at 85.9% for the opening week of March. Other markets, such as Sarasota (75.4%), Fort Lauderdale (72.5%) and McAllen/Brownsville, TX (70.5%), were lower but all above the 70% mark.

The following week provided a similar percentage of students on break, but Saturday, 13 March and Sunday, 14 March, is when things really began to heat up. Those dates showed the highest percentage of college students on break at one time (66%). Concurrently, roughly 32% of K-12 students were on break for the respective dates. During the second week of March, the Florida Keys market was once again on top in terms of occupancy (88.0%), followed by Daytona Beach (86.1%).