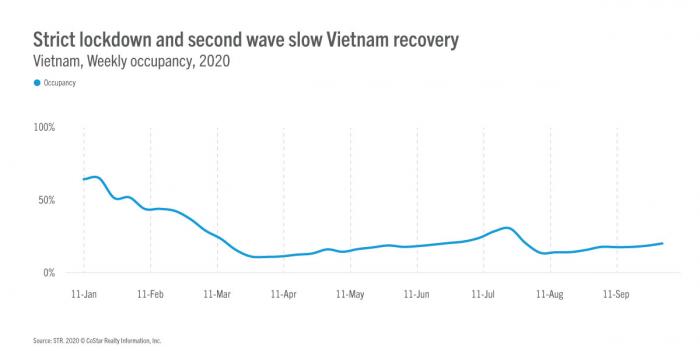

Next on our Asia Pacific tour, we check in with Vietnam, a country that hotel developers have watched closely in recent years. While the APAC region grew supply at 4.1% in 2019, Vietnam has emerged as a power player in the region, with over 5% supply growth in both 2018 and 2019. The country has handled the COVID-19 pandemic with aplomb, much to the detriment of the hospitality industry, but a thriving tourist trade and brand proliferation make the country one to watch once border reopen.

Developer darling

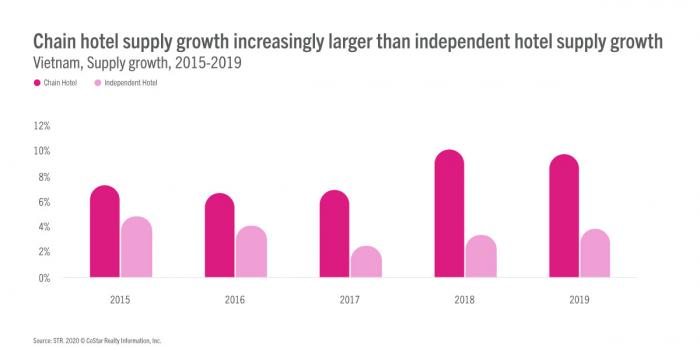

Vietnam’s hotel industry has historically been populated by independent properties: Nearly 73% of hotel supply was unflagged as of 2014. Brands have sought to change the status quo in recent years, and chain hotel supply growth increasingly outpaced independent hotel supply growth from 2015 to 2019.