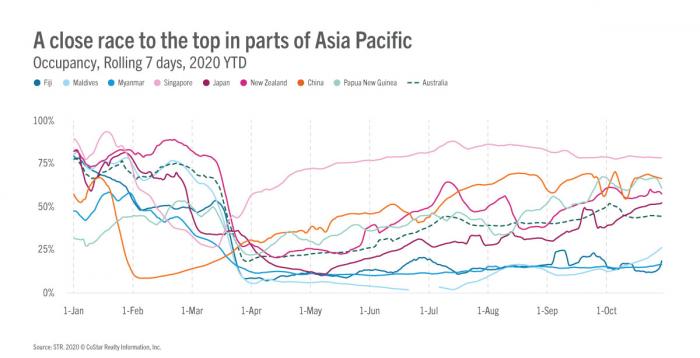

Hotel demand can be categorized into a variety of travel buckets: leisure and business, transient and group, and today’s focus, international and domestic. Recovery in the Asia Pacific region demonstrates the importance of that third bucket, as a country’s historic reliance on domestic demand directly impacts its hotel performance today.

Regional recovery can be divided into three tiers dependent on historical domestic demand and the state of the country’s borders today.