Previous analysis articles: SARS hotel performance recovery, Europe airport hotel analysis, Mainland China analysis

In this latest hotel performance analysis around the outbreak of coronavirus (COVID-19), we look at the impact in key Asia Pacific destinations for Mainland China travelers.

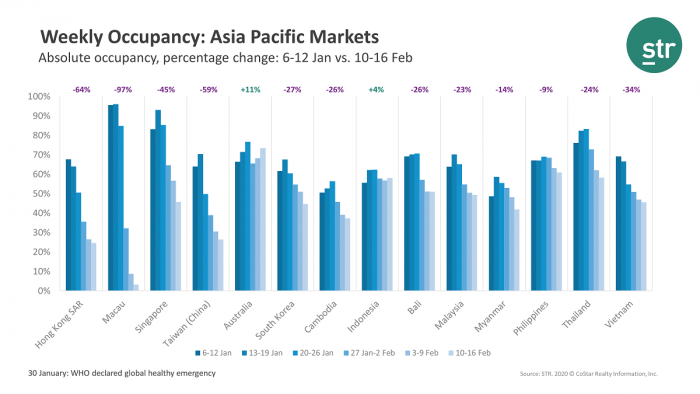

Using Tourism Economics’ global top 20 for Mainland China outbound travel, we analyzed 14 markets, some of which have seen a strong impact, many showing a moderate impact and some markets that have remained stable.

Markets included: Hong Kong SAR, Macau, Singapore, Taiwan, Australia, South Korea, Cambodia, Indonesia, Bali, Malaysia, Myanmar, Philippines, Thailand and Vietnam.

For the purpose of this analysis, we examined performance in the two weeks prior to Chinese New Year (6-19 January), the week of Chinese New Year (20-26 January) and the three weeks that followed (27 January-16 February). The weeks immediately after Chinese New Year have historically still included holiday travelers around the region.

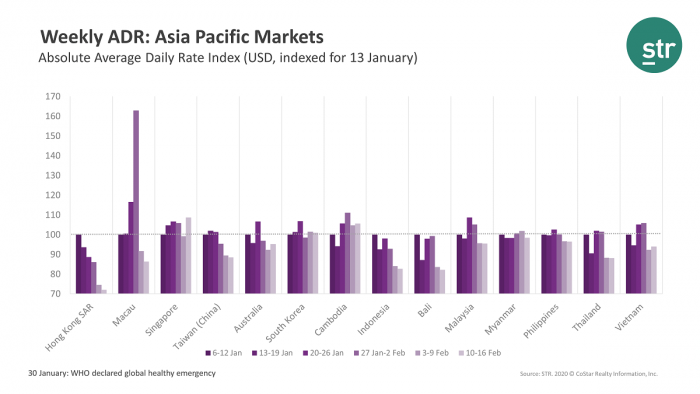

Please bear in mind that many of our ongoing reports on the performance impact of COVID-19 are based on daily data, which may differ from the total monthly numbers you will see at a later date. Given the extraordinary circumstances, we believe it is important to update you more frequently with preliminary data rather than wait for full-sample information. We omitted Japan from this prelim analysis due to differences in daily and monthly samples for that market. Japan will be covered in full monthly reporting down the road.

Occupancy

In general, we see high levels of occupancy the week before Chinese New Year, with hotel performance reflecting the push to complete business travel ahead of the holiday and school closings. For the week of Chinese New Year, we see a drop in occupancy, except in those markets which are popular holiday destinations for the Chinese traveler, notably Cambodia, Thailand and Australia.