As the impact of COVID-19 continues to affect hotel performance across the globe, the Middle East and Africa are no exception. At the time of writing, 52 hotel closures have been officially reported in the Middle East in addition to more than 1,200 in Africa. This is low, however, when compared to the just under 40,000 closings in Europe.

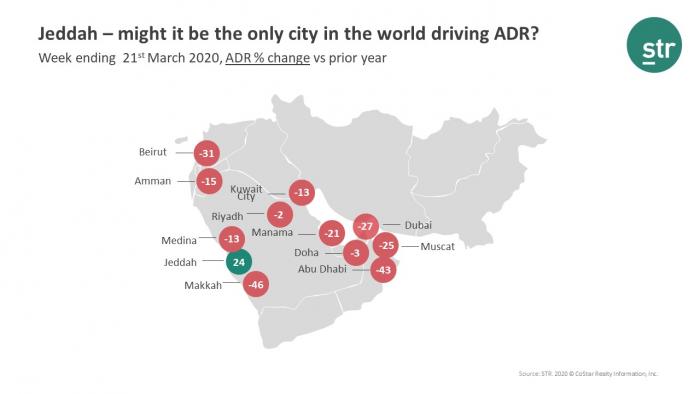

While many key global markets have reported occupancy declines exceeding 90%, Kuwait was the only Middle East market with an occupancy drop of more than 80% for the week ending 21 March. Others, meanwhile, have seen less severe decreases—such as Qatar (-30%) and the United Arab Emirates (-54%). To provide further insights, we’ve compiled five key findings from this 25 March MEA webinar.

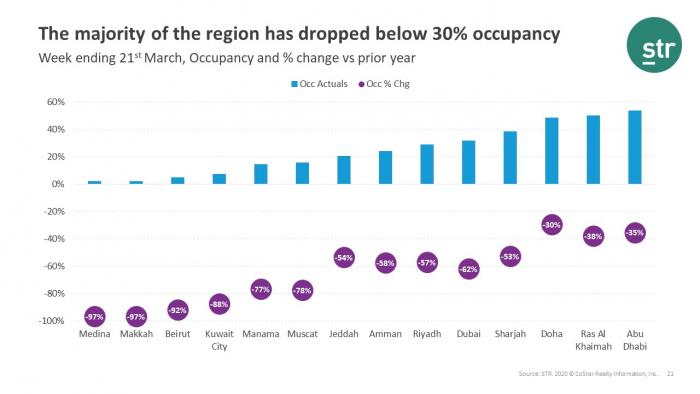

Declines have escalated in recent weeks

On a weekly basis, since the week ending 16 February, key countries in the region have reported progressively worse year-over-year occupancy declines. Unsurprisingly, several key Middle East markets have produced significant decreases, and the latest data—week ending 21 March—highlights that occupancy has fallen to below 30% for the majority. It is also worth noting that the two worst-affected markets are both in Saudi Arabia, following the declines that began with the suspension of Umrah visas on 27 February.