Analysis by M. Brian Riley

Driven by the surge in post-pandemic travel, overtourism became a major talking point across Europe in 2023 and continued to dominate discussions into 2024. With a year-plus of data now available, we can assess the effectiveness of various countermeasures and their impact on hotel performance.

Setting the stage

By 2023, the total volume of travelers to western Europe had mostly caught up with pre-pandemic levels, although the mix of travelers initially leaned heavily on the leisure side with a slower return of business travel. The mix remained somewhat skewed toward leisure demand in 2024, but the trend has moderated as corporate and group travel continues to gain ground in Europe.

Tourism remains a major economic activity for Europe, directly accounting for 10% of GDP according to the European Parliament. Tourism Economics estimates that in 2024 there were over 948 million visitors to western Europe, a 6% gain year over year and a roughly 7% increase above 2019. More than 55% of those visitors spent at least one night at their destination, with Americans accounting for more than 35 million of those total visits.

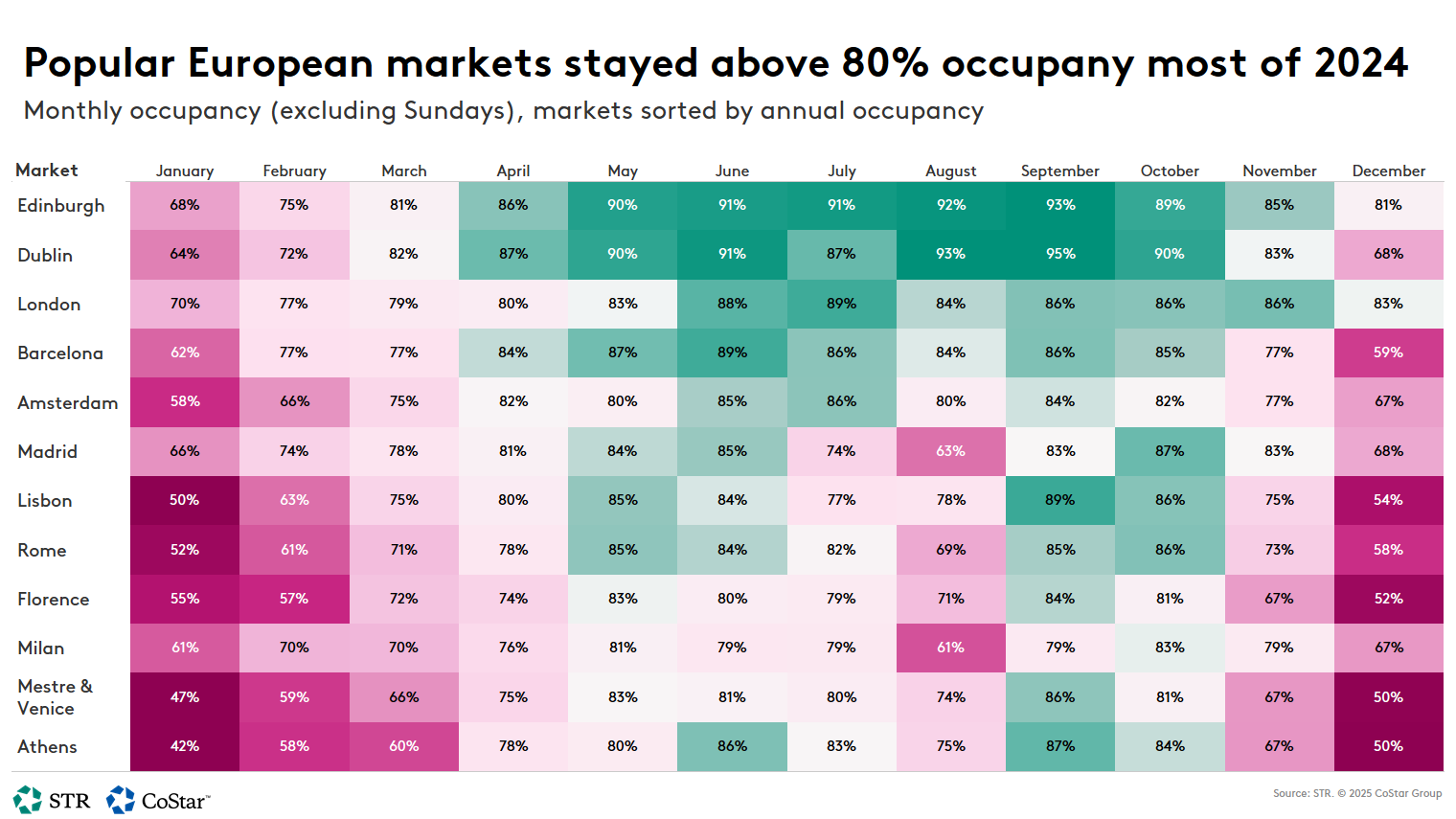

European market monthly occupancy (2023-24)

Monthly hotel occupancy patterns serve as an indicator of crowds and are evidenced in the heat chart below. Of note, this occupancy visual excludes Sundays, which are consistently the slowest performing night of the week.

- This select set of heavily touristed European markets runs comparatively high occupancy for a large portion of the year, similar to pre-pandemic years. High seasons demonstrated consistent occupancy levels near or above 80%.

- All markets show strong seasonality patterns. September was the top ranked occupancy month for six of the 12 markets. Athens posted the largest occupancy deltas between its peak months (June, September) and slow months (January, December).

- More business-centric hubs, such as Edinburgh, London and Dublin, showed longer peak occupancy seasons with high room demand/occupancy extending into shoulder months beyond summer.

- Monthly occupancy was highly consistent between 2024 and 2023. The data provides no evidence of any occupancy shift outward from peak to shoulder months.

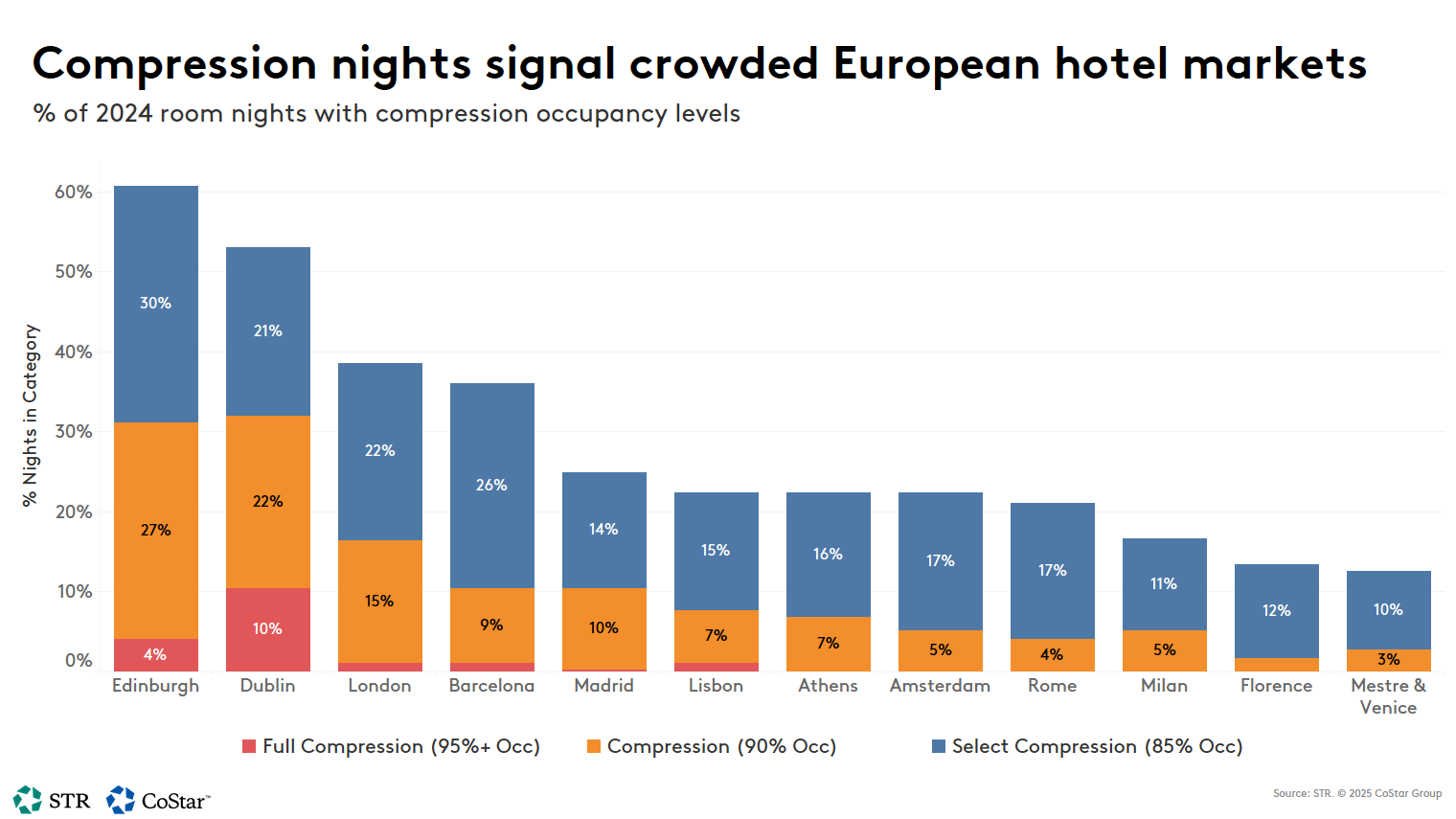

Number of compression nights remain relatively high

High daily occupancy levels provide a clear signal that there may be a glut of room demand in comparison to a hotel market’s existing room supply. This serves a catalyst of strong growth in average daily rate (ADR).

A loose categorization of occupancy-based compression is as follows:

- Select Compression (Market Occupancy >85%): Individual hotels as well as more desirable locations within the larger market may be full. Still, vacant rooms are readily available.

- Compression (Market Occupancy >90%): Most sections/submarkets of a large market have reached or are nearing their full demand capacity. Last-minute travelers may be pushed to outer lying submarkets and properties.

- Full Compression (Market Occupancy >95%): The market is nearing its maximum capacity, and it is challenging for any last-minute traveler to locate an available room.

Edinburgh, Dublin and London hotel markets reported the most nights with compression-level occupancy. Edinburgh led 2024 with 61% days in the compression zone, followed by Dublin (53%) and London (39%).

Six of the 12 heavily touristed European markets saw declines in the number of compression nights between 2023-24. The decreasing markets included Athens, Barcelona, Florence, Lisbon, Milan and Rome. The sharpest declines occurred in Florence, which reduced its total number of compression nights in 2024 to 49 from 74 in the prior year (-34%). Athens’ 2024 compressed nights decreased 11% to 82, while Barcelona reduced compression nights 5% to 132.

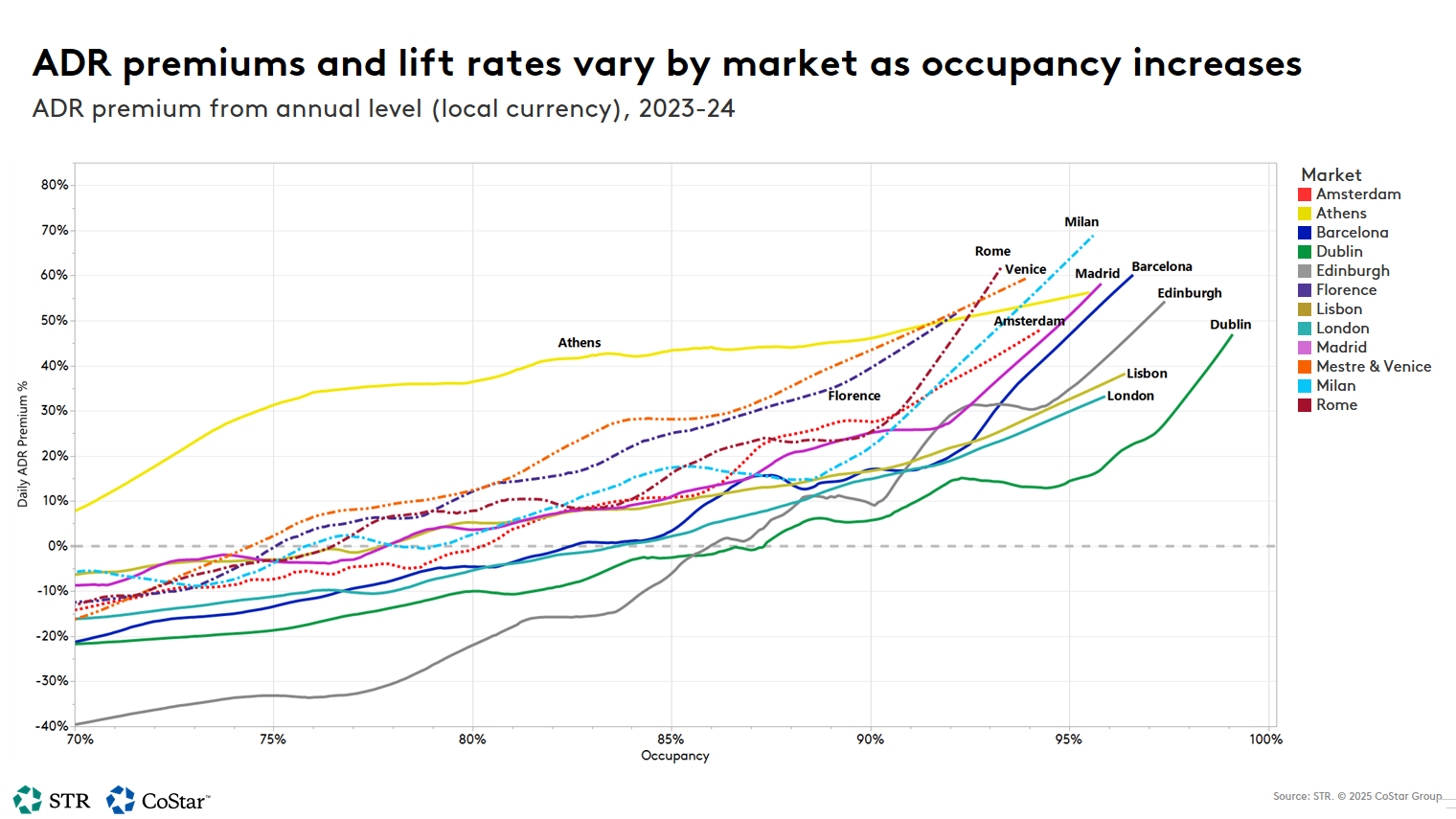

Occupancy impact on ADR in heaviest touristed markets

A common question among hotel operators within highly touristed markets is what degree higher occupancy benefits the bottom line through added room pricing power. The following chart demonstrates enhanced regression lines to each market with ADR percentage premiums (percentage indices against a market’s own yearly ADR) being compared to occupancy on days when the occupancy is 70% or higher. These curved models identify key compression points when, on average, area operators increase ADR.

There is an uneven nature to potential rate gains as occupancy increases. In other words, those last rooms sold within a market often sell at a higher premium than the market’s initial room inventory around a demand-driving event. It is typical for markets to see large “turbocharges” or jumps in their ADR percentage gains within a short span of growing occupancy – these thresholds are indicative of market compression.

- In all cases, higher occupancy shows a positive relationship with ADR levels.

- ADR premiums appeared earliest in Athens due to seasonal closures and steeply discounted rates during the four-month low season from November to February. When tourist season picked up, however, Athens saw almost no compression-driven bumps in ADR.

- Venice, Lisbon and London are other markets that showed more linear and less bumpy relationships between ADR and occupancy once daily occupancy surpassed 75%.

- The remaining European markets demonstrated more typical compression-related ADR jumps. The greatest ADR lift rates occurred after market occupancy surpassed 90%.

These European destinations demonstrated differing paces of ADR gains (general slopes from trends) above baseline levels but also show distinct occupancy thresholds when ADRs jump to higher premiums.

Several markets show little evidence of large ADR boosts when experiencing higher occupancies. One potential factor minimizing ADR growth may be price sensitivity, particularly among budget-minded leisure travelers. As normally elevated seasonal rates peak, the added costs beyond room rates may compel this category of traveler to look for discounts or otherwise consider other destinations or alternative accommodations. Likewise, local hotels may feel pressure to minimize ADR premiums to maintain demand.

Closing observations

Popular European destinations have greatly benefited from the post-pandemic rebound in tourism. Hotels are core beneficiaries with recent peak seasons providing exceptional occupancy which, in turn, drives substantial ADR growth. However, the gains from increased tourism often come with large social and economic costs. Most notably, resident-led protests in the tourist centers of Barcelona, Venice and Amsterdam over the past few years have made international news.

Local authorities in some markets have taken actions to temper overtourism especially during peak seasons in the hopes of reducing crowds. Many popular destinations have already raised lodging taxes or otherwise are considering adding taxes and tourist-centric fees. Last year, Amsterdam implemented one of the world’s largest bed taxes. Venice enacted a tourist tax of up to €10 for all day-trippers in 2024. In January, Edinburgh became the first market in the United Kingdom to implement a special room tax (5%), which goes into effect in 2026, and will support heavily touristed facilities.

Perhaps as an extreme case, the city of Venice, and its 49,000 residents, saw 30,000,000 visitors in 2024 despite the addition of a €5 tourist fee for day-trippers during peak periods. Venice’s annual occupancy increased 1.3 percentage points YoY (to 70.1%) in 2024, further evidence that travelers appear to not be dissuaded by extra measures to control overcrowding.

Amsterdam’s 2024 results are a more mixed picture as the market continues to see small increases in annual occupancy (+0.5ppt to 75.7%) as well as the number of crowded (compression-impacted) days (from 77 to 83 days). At the same time, the market’s 4.5% drop in its ADR hints at added pressures felt by hoteliers to draw increasingly price sensitive leisure travelers who are being hit by significant costs outside of room rates. Amsterdam raised its tourist tax to 12.5% (+7%) in 2024 and has additional plans to raise its broader VAT tax to 21% in 2026.

Despite some added measures, data for these select European markets did not show consistent shifts in demand and peak season overtourism in 2024. While many markets have taken the first steps to reducing overtourism, traveler interest in European holidays is unlikely to wane. Most European markets, including Amsterdam, Barcelona, London and Rome, anticipate continued occupancy growth in 2025.