Miami/Hialeah, Florida, the 2020 host market, is projected to reach a record hotel average daily rate (ADR) level during the event weekend – between US$520 and US$540 for Friday, January 31 through Sunday, February 2. The market will be starting from a higher basis because of the already high rates in the market. Miami is also expected to be among the top performers in terms of absolute occupancy, with a forecasted range of 91-94% during the 3-day period.

Miami last hosted a Super Bowl in 2010, but the landscape has changed drastically since, as around 10,000 additional rooms have entered the market, and the economy likely played a part in 2010 ADR levels.

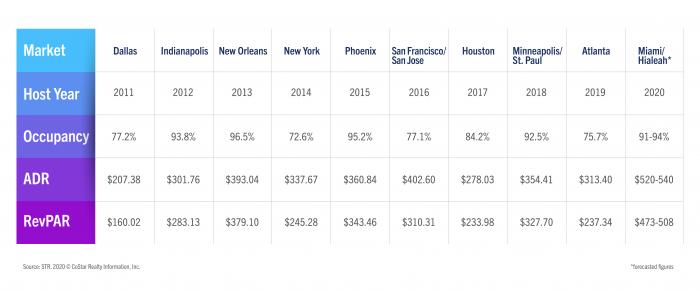

This leads to the question of how other host markets over the last decade performed, and what can their performance tell us about the Super Bowl’s effect?