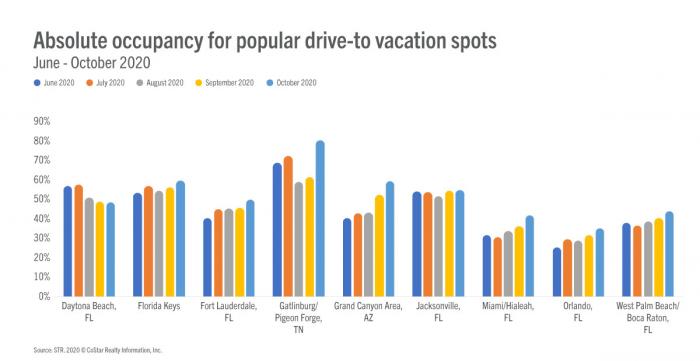

In a recent blog post, we covered how the summer months provided U.S. hotels with an increase in leisure travelers, a welcome change that lifted the industry from the pandemic performance lows of the spring. Naturally, we expected that leisure travel to dry up and overall hotel performance to retreat due to the return to school and a persistent lack of corporate and business travel. However, a closer look at September data from a variety of popular vacation spots showed that some markets extended that leisure-driven performance into the early fall and even outperformed the same month last year. It appears that many leisure travelers made the most of the remaining warm weather, ahead of possible new COVID-19 travel restrictions around the country.

For this analysis, we focused on some of the top drive-to vacation spots as a major trend this year has shown travelers hitting the road rather than fly amid a pandemic. We looked at several Florida beach markets, the Gatlinburg/Pigeon Forge, Tennessee submarket, and the Grand Canyon Area submarket in Arizona.