After reaching its pandemic performance lows in April, the U.S. hotel industry saw performance climb during the summer months, helped by weekend leisure travel, especially in drive-to destinations. With a post-summer slump evident in weekly data through October, we look back in time to find some brightness in the data.

By Month

Summer was already off to a good start in June, when occupancy reached 42.2%, up from 33.1% the month prior. Occupancy stayed well above the 40% level throughout the summer months, with August producing the highest occupancy since the start of the pandemic at 48.6%. That rate held through September at 48.3%.

Average daily rate (ADR) and revenue per available room (RevPAR) followed suit, with both metrics reaching the highest absolute levels in August, at US$102.64 and US$49.91, respectively.

Each month between April and July, the year-over-year RevPAR % change improved by 10 percentage points, however between July and September, the percent change in the metric barely fluctuated and is expected to stay fairly muted throughout Q4 as there is still no corporate group demand. Over a million group rooms were sold in August and September, due in part to weddings, sports teams, etc., as opposed to the pre-pandemic world in January when over 6 million group rooms were sold.

While the above data is for open hotels only, it is important to note that Total-Room-Inventory occupancy (which excludes temporary closures due to the pandemic) did not differ by much from the standard occupancy during September. Standard occupancy stood at 48.3%, while TRI occupancy was 46.4% – a difference of 4.0%.

By Market

A mix of U.S. markets saw their fair share of stronger summer performance. In June, beach drive-to destinations rose to the top of the occupancy charts, with five of the top 6 markets reflecting a “sand- between-your-toes” feel. Those markets included: Myrtle Beach, S.C. (63.1%); the Florida Panhandle (62.5%); Mobile, Alabama (59.2%); and Daytona Beach, Florida (57.0%).

The next few months were led by different markets, with Colorado Springs outperforming all other U.S. markets in occupancy during July (69.8%) then ranking second among all markets in August (74.0%). McAllen/Brownsville, TX, led the markets in the metric in August (80.0%) and September (71.4%).

By Class

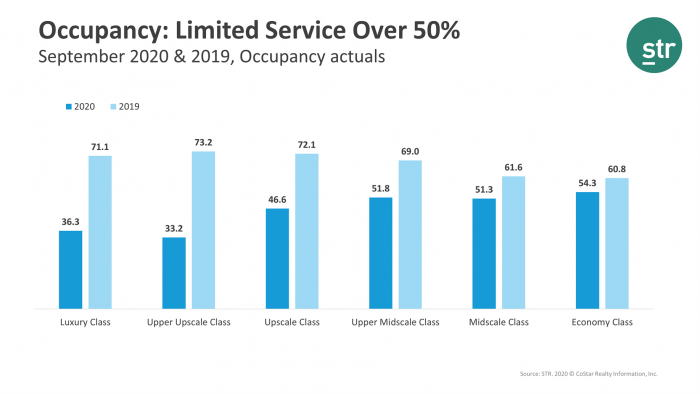

As group demand is virtually nonexistent, it is no surprise that the lower-end hotels have been outperforming the higher-end hotels. Led by the Economy class, limited-service hotels have reported occupancy levels above 50%.