Website update in December We’re pleased to announce a streamlined customer journey with the integration of str.com into costar.com. Beginning in early December, any visit to str.com will be rerouted to costar.com. To enter property data or access the STR Client Site, log in here or via the Benchmark page of costar.com. More details here. Learn More.

In the first instalment of this series, we concluded that the looming shadow of Brexit had little impact on hotel performance in the U.K. That analysis was supported by continuing year-over-year growth in both occupancy and average daily rate (ADR) in 2018. However, a lack of change in performance trends in the market made it necessary to dig deeper into the story to analyse whether or not profitability has been affected.

Image

London driving profitability growth for overall U.K.

With healthy growth in revenue per available room (RevPAR), the U.K. enjoyed an overall increase in total revenue per available room (TRevPAR) of 3.5% in 2018, compared to departmental expense growth of 3.1%.

Breaking this down by department, rooms reported the largest revenue growth in actual terms, up GBP34,557 per available room or 3.8%. Food and beverage (F&B) also rose 1.1%, driven by Other F&B (+1.2%). Expenses increased at a lower rate than revenues resulting in an overall GOPPAR increase of 3.0%.

Image

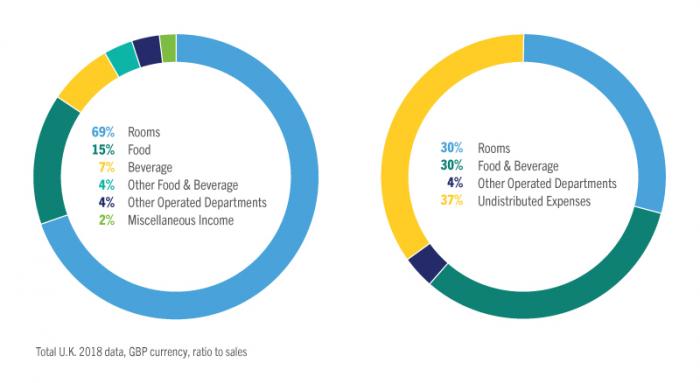

Rooms revenue in the U.K. accounts for 69% of total revenue while F&B accounts for 26%, following a similar trend to that seen in Europe, where rooms account for 70% and F&B for 26%.

Of total expenses, undistributed expenses account for the highest proportion (37%) and a similar trend is evident in Europe.

London growth is outpacing the Regional U.K.

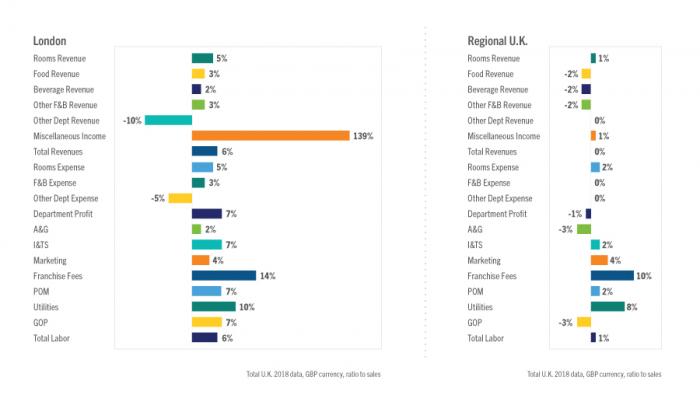

While overall U.K. performance is positive, digging a little deeper tells the story of a thriving capital city and a struggle in other regions. London drove U.K. performance in 2018, as occupancy and ADR growth exceeded year-over-year growth expectations. Regional U.K., however, reported relatively flat RevPAR performance (+0.5%). The chasm between the two can be seen in the image below.

Image

Revenue and Expense Performance

London’s increase in total revenue (+5.6%) can largely be attributed to a lift in room revenue (+5.4%), although almost all revenue line items showed growth—apart from the 9.7% decrease in other operated departments. Regional U.K.’s drop in TRevPAR and GOPPAR is a symptom of declines across all revenue categories excluding rooms. F&B showed the most notable decrease, falling 1.7% against the previous year.

As departmental expenses rose just 0.2%, London closed 2018 with 6.5% year-over-year growth in departmental profit. With total revenue falling and total departmental expenses (+1.1%) rising slightly in the Regional U.K., there is an indication that hoteliers struggled to reduce costs. This is reflected in the ratio-to-sales figure, where departmental expenses accounted for 34.8% of total revenues in London versus 42.8% in Regional U.K.

Labour cost growth was reported in both London (+6.1%) and Regional U.K. (+1.0%), with the increases driven by different areas. London’s largest lifts came in information and telecommunication (+11.3%) as well as property operations and maintenance (+9.2%), suggesting additional investments were implemented for properties to remain competitive. Regional U.K. recorded the largest increase in marketing (+5.0%), demonstrating a need for hoteliers to improve the attractiveness of the region. According to Reuters, U.K. labour costs across all industries were at their highest level for the last five years in late 2018. With the unemployment rate at its lowest since the 1970s, employers are struggling to retain staff.

Franchise fees and utility costs were the fastest growing undistributed expense items in both London and the regions. This is also reflected in an increase in the Consumer Price Index (CPI). Oxford Economics reported 2.5% growth in the CPI against the previous year. With the CPI projected to grow, utility costs are likely to rise in the coming years. As utility costs mainly comprise energy-related expenses, the increase can also be attributed to occupancy growth. Breaking down the U.K.’s growth in franchise fees, London and Regional U.K. recorded 14.1% and 9.9% increases, respectively. Franchise fees comprise three components that can be retrieved through an in-depth analysis of undistributed expenses: franchise royalty fees, franchising and affiliation advertising, and loyalty programs and affiliation fees. The 2018 increase in franchise fees was predominantly driven by royalty fees. Recent research supports this, highlighting a growing trend towards the franchise model, and our hotel supply and pipeline database showed that 59 properties across the U.K. opened under or transitioned to a franchise agreement model in 2018 .

Brexit yet to affect hotel profitability

So far, so good in terms of hotel profitability, as Brexit is yet to have a noticeable impact in London, although growth has slowed for the overall U.K., and the trends identified here are likely to continue in the coming years. The fundamentals for demand growth remain valid, and the U.K. is expected to reach 40 million visitors by 2023 with a CAGR of 2%, which will likely result in higher revenue for hoteliers (Source: Oxford Economics).

In terms of profitability growth, hoteliers can take action on their bottom line by aiming for rate-driven increases, as occupancy-driven growth increases owner consumption costs. An earlier analysis from STR revealed that “for the [the UK-based] hotels in this study, rate performance had a greater impact on overall profitability than occupancy performance”.

The future of U.K. profitability depends on the type of deal that the U.K. makes with the EU. While a no-deal scenario has a 35% probability, it is expected to lead to higher inflation and a subsequent weakening of the Sterling in the short term (Source: Tourism Economics). This could affect import prices, the cost of food, and health and insurance premiums alongside more complex Visa regulations and labour costs. Although this is a worst-case scenario, it highlights Brexit’s potential impact on hoteliers. Year-to-date RevPAR for 2019 reported declines in Regional U.K. and suggests additional pressure on profitability in the future, while London remains resilient.

*growth per available room, based on a consistent sample of 423 properties.