July and August are two of the most important months for hotels in the United Kingdom with travelers spread across the country as part of their summer holidays. However, it is no secret that summer looked much different this time around due to the global impact of the COVID-19 pandemic.

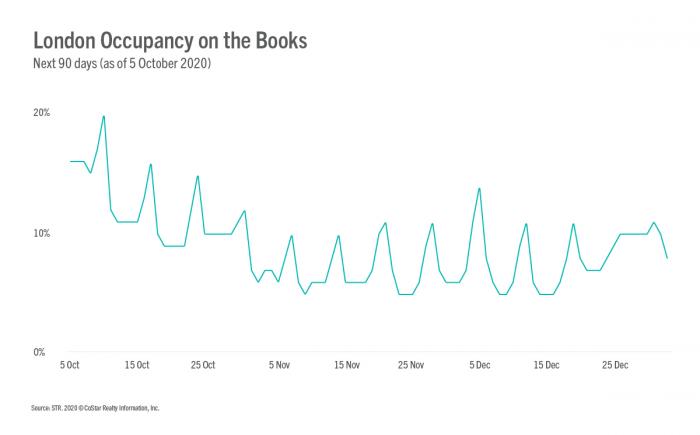

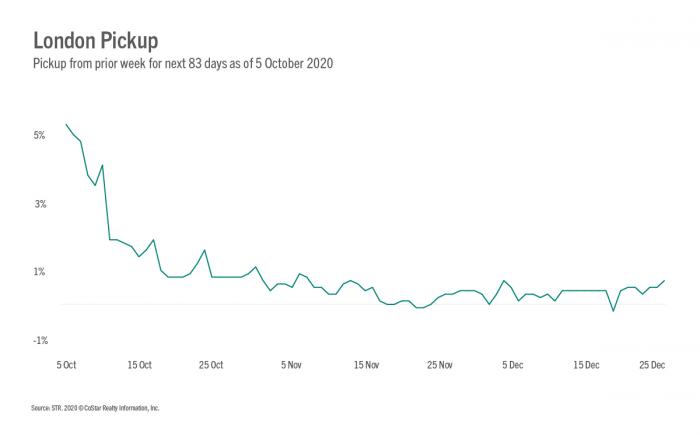

As more recent performance reflects the return to school and continued lack of corporate and events business, we look back at the impact of leisure holidays on the U.K. summer then look ahead with data powered by Forward STAR.

At the time of writing this blog, new lockdown measures were being announced thanks to high alert levels in London, Manchester, and several other areas in the country. This further complicates the performance picture moving forward and highlights the need for benchmarking the future.

Staycation impact

The U.K.’s 57% occupancy level for the week ending 30 August was its highest since lockdown began. Thanks to summer holidays, leisure markets were the driving force behind rising occupancy levels. On Saturday, 29 August, the U.K. Regional market reached an occupancy level as high as 75.7%.

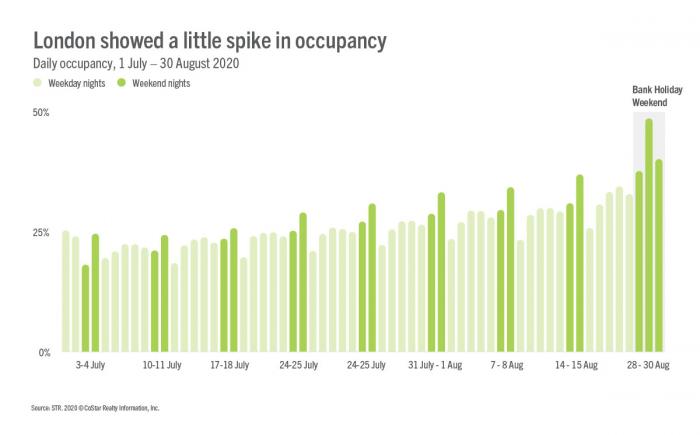

Data for the same week showed occupancy at just 35% in London, indicating some demand flowing into hotels, but at a limited rate. During the bank holiday, London posted an occupancy level as high as 48.7% on 29 August. This indicated more demand driven by domestic sources.