About the MRM

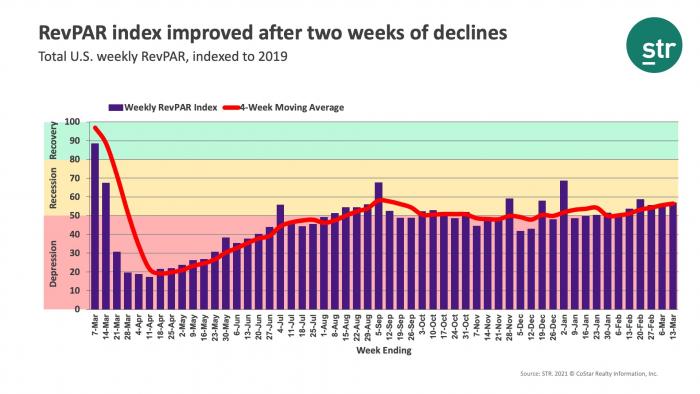

When the U.S. hotel industry reached the one-year anniversary of the earliest COVID-19 impact, year-over-year percentage changes became less actionable when analyzing performance recovery. Thus, STR introduced a weekly Market Recovery Monitor that categorizes each STR-defined market based on an indexed comparison with the same time periods in 2019. An index is simply a ratio that divides current performance by the benchmark (2019 data).

For example, during the week ending 6 March 2021, U.S. RevPAR was $48.13. In the comparable week from 2019, RevPAR was $87.75. This produces an index of 54.8 ($48.13/$87.75*100), meaning RevPAR was slightly more than half of what it was in 2019.

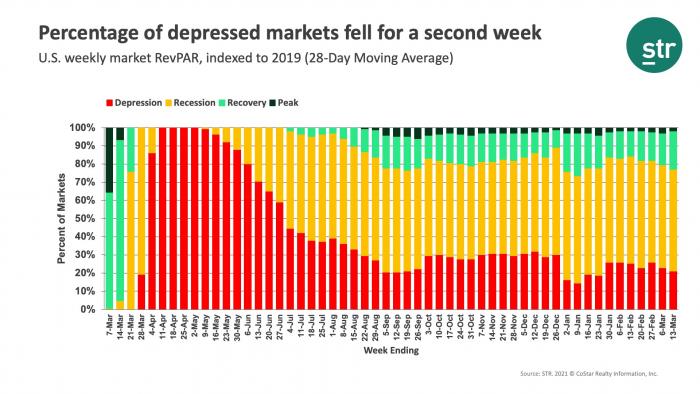

We use an index to place each market in one of four categories: depression (index <50), recession (index between 50 and 79.9), recovery (index between 80 and 99.9), and peak (index >=100). Additionally, we highlight other top market performances that contribute to higher levels of recovery across the U.S.

Week Ending 13 March 2021

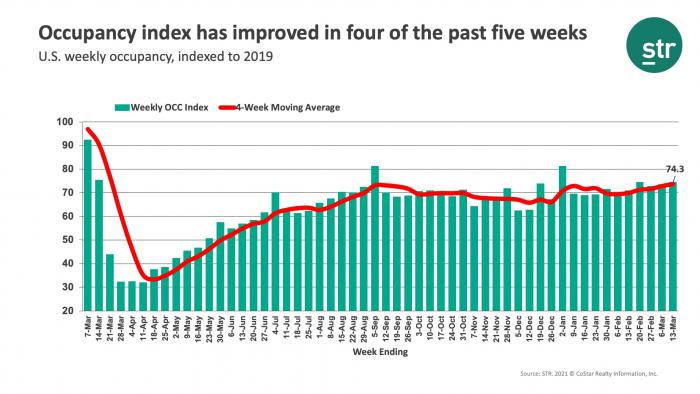

The U.S. achieved its highest absolute weekly RevPAR ($53.45) since the week ending 14 March 2020. A year-over-year decline of 15.8% was the smallest since the start of the pandemic. However, a lessening of the year-over-year decrease is mostly a function of an easier comparison. When indexed against 2019, RevPAR was 57% of the level achieved during the comparable week in 2019. Similar to the most recent weeks, that RevPAR index remains well in the recession classification.