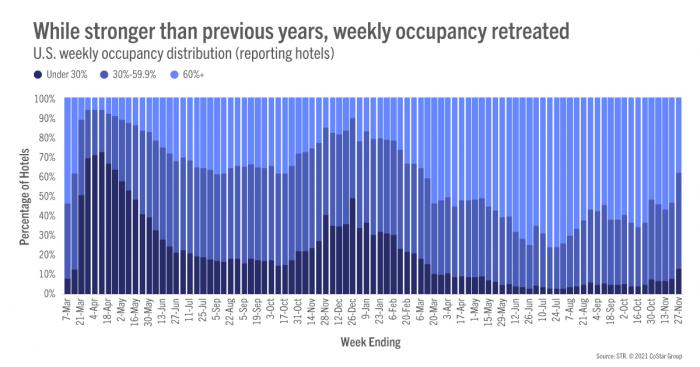

Thanksgiving week for the U.S. hotel industry was record-breaking by all measures. Weekly occupancy topped 53%, which was 2.3 percentage points higher than the holiday week in 2019 and nearly a point higher than the previous record achieved in 2018. Thanksgiving Day occupancy (56.9%) fell a bit short to 2018’s level (57.3%) as did Monday’s, but occupancy on the other days of the week were at record highs. Looking at the 3-day weekend (Thursday to Saturday), occupancy reached 60.2%, 0.9 percentage points greater than in 2018 and 2017 which had been the bar to surpass. Weekend (Friday and Saturday) occupancy (62%) was also at a new high for the week of Thanksgiving.

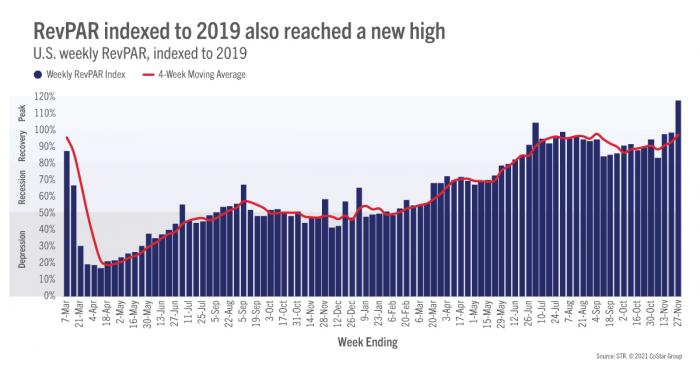

More than 20 million rooms were sold during the week with every day of the week posting a Thanksgiving week record. As compared with Thanksgiving week 2018, the previous record holder, most of the demand gains were seen in upscale and upper midscale hotels, particularly in suburban locations, which makes sense as these hotels are closest to residential areas. Upper upscale hotels saw the largest deficit against 2018, particularly in urban locations. Likewise, independent hotels in urban locations saw a sizeable decrease in demand for the week as compared with 2018. We also noted a decline in demand among resort location hotels across most of the chain scales except upscale and luxury. Overall, demand for the week was at a record high for all locations except urban and resort, although resort location occupancy was the highest (60%) of any location for the week. With the sharp increase in demand, weekly industry occupancy indexed to 2019 increased to 104.6, the highest level since the start of the pandemic. The index has increased in five of the past six weeks with November on track to have the second highest occupancy index of the year, behind only July.