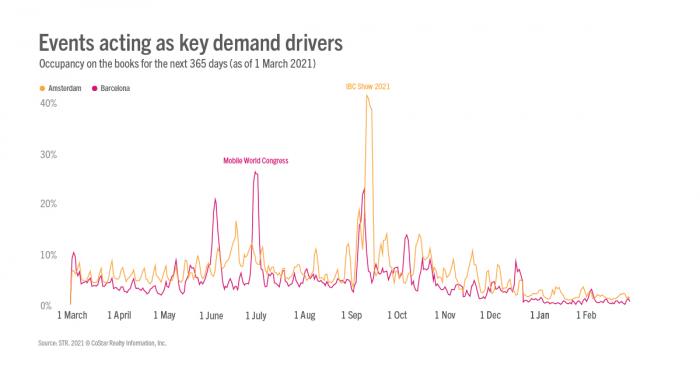

When will customers have the confidence to book 12 months in advance? When will events return with notable capacities?

As we’ve seen in a previous article, booking windows have significantly decreased since the beginning of the pandemic. In this latest article, we analyzed two of the major contributing factors to the reduction of booking windows: current volatility and consumer confidence.

Current Volatility

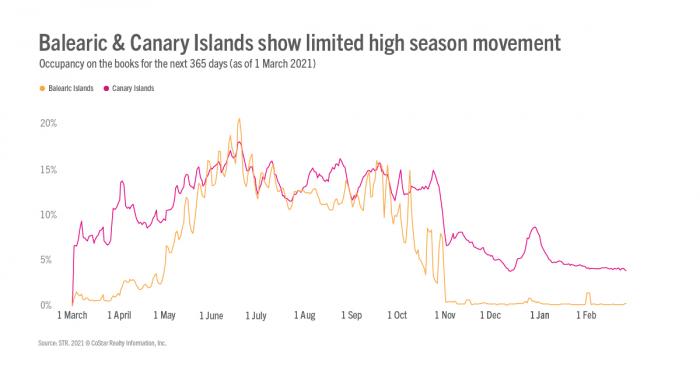

To assess volatility in bookings, we focus in on Forward STAR data for a pair of markets in Spain.

For May through October 2021, the Canary Islands’ occupancy on the books remains between 10-20%, and beyond those months, the metric stays below 10% with only occasional lifts. The Balearic Islands’ follows a similar pattern with limited movement for high season (June-August). While slight rises pop up, occupancy on the books remains below the 20% level for most of high season. As of 1 March, the market’s highest levels in occupancy on the books were just 20.1% (19 June) and 20.7% (17 June).

However, it is important to note that the pandemic has shifted guest tendency toward shorter booking windows. An uptick in leisure travel, especially domestic leisure travel, could push levels higher in the upcoming months.