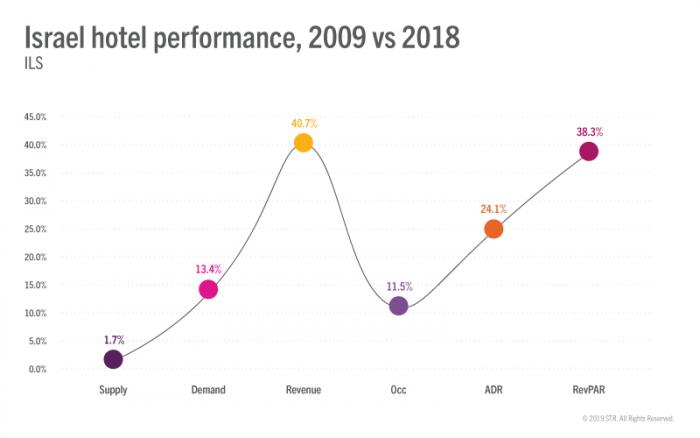

In the below article we will undergo a deep-dive analysis of hotel performance across the country and its key markets. STR’s hotel sample in Israel has continued to grow in the past decade, particularly over the last year. STR’s Israel sample now comprises over 100 hotels which represents 24,000 rooms, enabling us to closely and accurately analyse trends within each of Israel’s diverse hotel markets.

Israel across the board

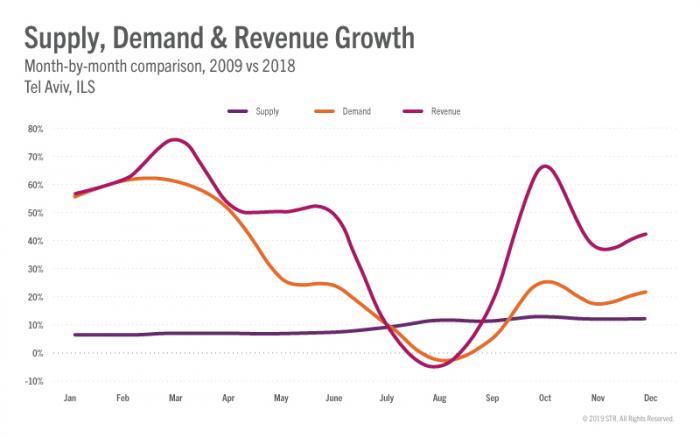

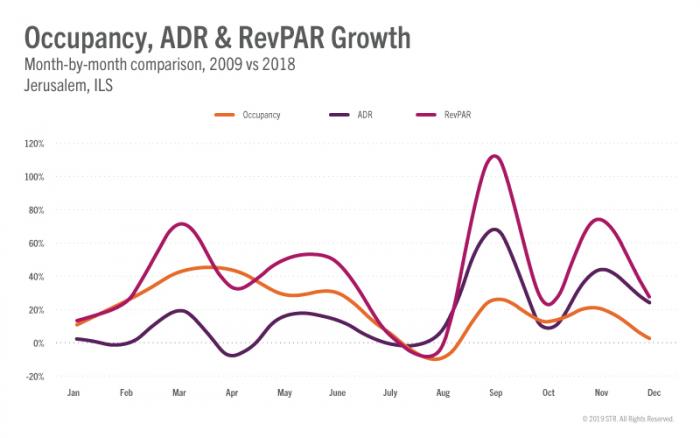

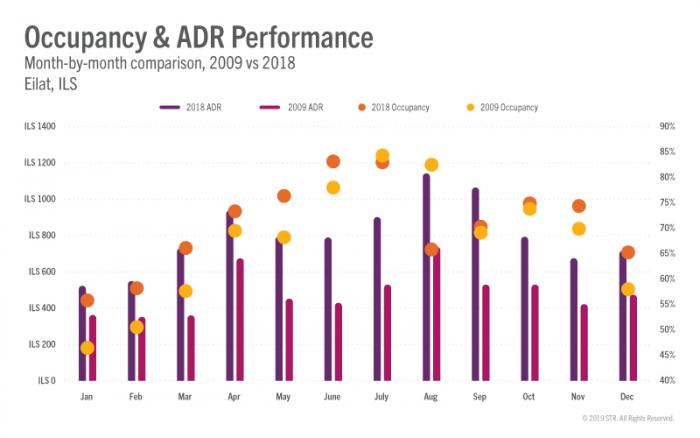

A decade ago, Israel hotels would be at their busiest during the summer months. Today there is a shift in this trend, especially during August where occupancy has dropped 19.7% between 2009 and 2018. Average daily rate (ADR), however, increased 18.0%, although we have to take currency fluctuations over this period into account. This shift in performance, as well as supply and demand, has generated a 3.4% loss in rooms revenue during August since 2009.

On the other hand, the low and shoulder seasons have seen double-digit growth in demand and revenue. March has seen the strongest hotel revenue increase (+74.2% to ILS836,729,848). Higher occupancy levels in January and February helped push RevPAR, +36.1% and +48.6%, while revenue rose 38.6% and 51.1%, respectively. Demand growth also surpassed supply in February (+38.6%) and March (+37.2%), while supply grew by just 1.7% and 1.8%, respectively.

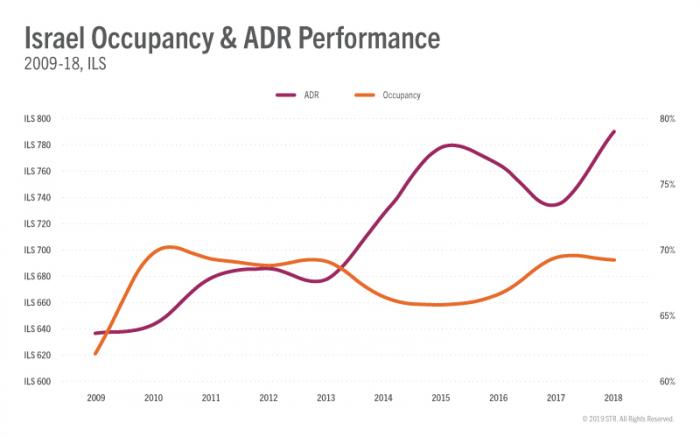

Overall, Israel has seen healthy build up in RevPAR performance, as seen in the graph below. This growth has been driven by occupancy increases between 2009 and 2013, and from 2014 onwards hotels have relied on ADR growth to achieve RevPAR increases.