STR continues to monitor the hotel performance impact around the outbreak of novel coronavirus (2019-nCoV). To this point, we have focused on the immediate impact in Mainland China and key outbound destinations in the Asia Pacific region.

Next we examine Europe, which according to Tourism Economics, welcomes 15% of Chinese outbound travel. That number is of course much smaller than the 80% of Chinese outbound travel that stays within the Asia Pacific region, but several countries in Europe are key destinations for the Chinese traveler. Within Europe, France, Russia and Germany are the top countries for Chinese arrivals.

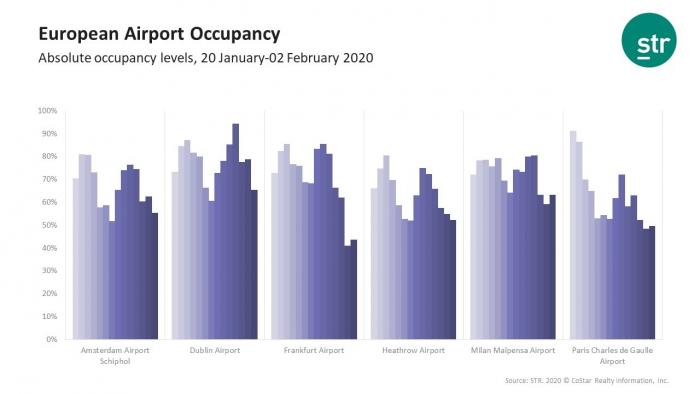

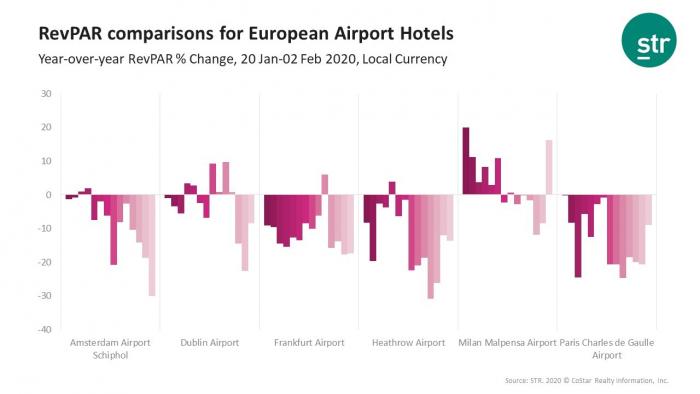

In examining key markets around Europe, we have not yet seen a noticeable impact on overall hotel performance. However, an impact is visible in specific locations: airport hotels. As a reminder, STR defines airport hotels as those properties in close proximity to an airport that primarily serve demand from airport traffic (distance may vary).

For the purpose of this analysis, we look specifically at Heathrow Airport, Paris Charles de Gaulle Airport, Frankfurt am Main Airport, Dublin Airport, Milan Malpensa Airport and Amsterdam Airport Schiphol for the two-week period between the 20 January and 2 February.

Notable dates to remember are 24 January (Chinese New Year day), 30 January (global emergency declared by the World Health Organization) and 28 January (various international carriers began cancelling flights in and out of China). Many of these airlines, such as British Airways, Lufthansa and Air France, have suspended flights until the end of February or end of March.