Did you miss one of our webinars? Don’t have time to watch the full recording? No problem. We are pleased to present the key points in this latest COVID-19 webinar summary. In this edition, we talk performance in France.

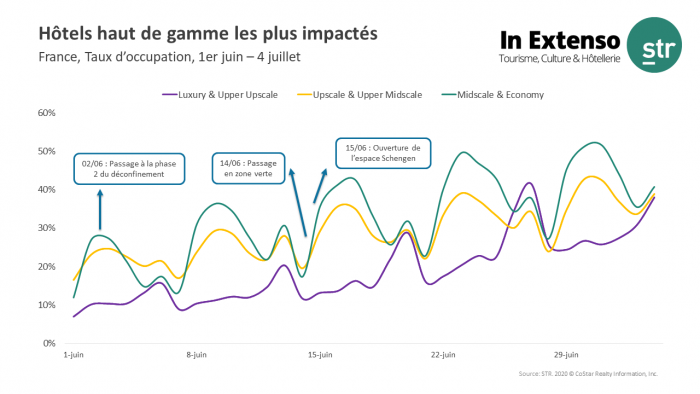

Luxury and Upper Upscale Class hotels the most affected

All hotel classes in France have been impacted by the COVID-19 pandemic, however, the Luxury/Upper Upscale segment has been the most affected. On 1 June, Luxury/Upper Upscale hotels sat at 7% occupancy, but by 27 June, the segment had grown to 41% occupancy—a maximum in recent weeks. For comparison, Midscale and Economy posted its highest occupancy level of 51.7% on 1 July.