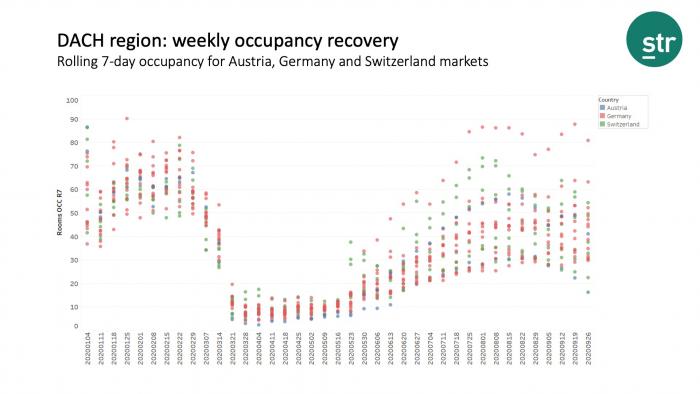

Adapting to shifts and fluctuations in demand has always been a key advantage in moving hotel performance forward. Following a pattern similar to markets in other parts of the world—like China—the DACH region (Germany, Austria and Switzerland) has managed to recover its occupancy at a faster pace than most markets in Europe.

In March, and particularly April because of government regulations, performance in the region dipped to an all-time low amid the COVID-19 pandemic. Hotels were not forced to close completely, however, and remained open for business travel as leisure tourism stalled. Germany’s occupancy fell to just 8.2%, while Switzerland and Austria dropped to 8.9% and 4.6%, respectively.