Tourism arrivals can drive significant inventory growth

The Middle East has undergone a tourism evolution in the past 10 to 15 years, highlighted by recent arrival figures. In 2019, the Middle East reported 64 million international tourist arrivals (which represented 8% growth year over year), and it was recently reported that they will reach 150 million visitors annually by 2030 (source: World Tourism Organization). Understandably, all these additional travelers need a place to stay, and this is reflected in hotel inventory.

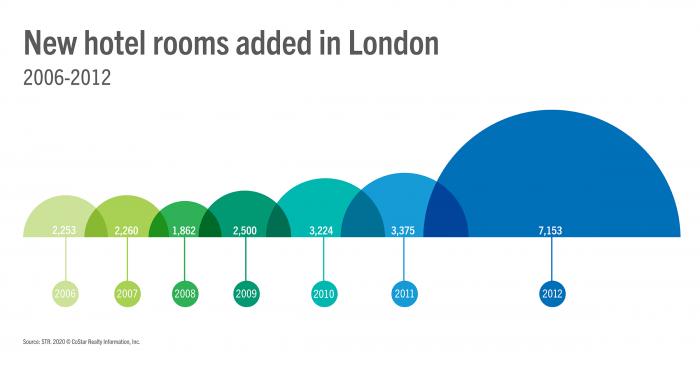

We’ve used Dubai as a case study to illustrate this point and, between 2006 and the start of 2020, the market’s available inventory has increased 140%. To add context to this, London has risen just 33% in the same period. Over the last ten years, a total of 159 hotels and 48,399 rooms have opened in the emirate—representing 65.2% growth on the 462 hotels and 74,203 rooms available during the start of 2010. Inventory will continue to grow with tourism, and there are just over 60,000 rooms in Dubai’s under contract pipeline at time of writing.

Mega events mean mega room growth

Landing a major event is like hitting the jackpot, with a significant influx of visitors almost guaranteed for that brief period, and the majority needing somewhere to stay. From a hospitality perspective, confirmation of a host city often raises questions and opportunities to ensure the accommodation infrastructure can support the event.

As we discussed one year ahead of Euro 2020, the impact of sporting events can significantly impact room openings. Copenhagen would welcome a 20.0% increase on existing inventory in less than three years leading up to the event, while Bilbao opened its first rooms since 2011 in preparation for kick off.