Scotland’s hospitality industry has undergone change in recent years, with some markets experiencing success as others have declined. But what are the factors and stories driving these changes? We’ve taken a look at 2019 performance and recent trends in a number of key markets in order to answer these questions.

From Aberdeen’s oil crisis to the rapid rise of Dundee tourism, this two-part series is your key to understanding Scotland hotel performance and market development.

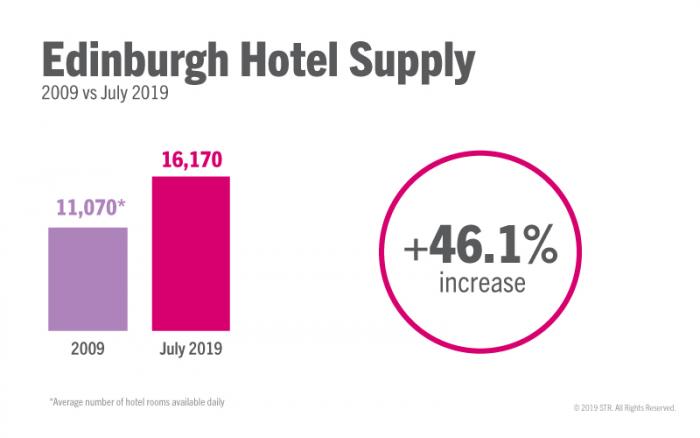

Edinburgh

The Scottish capital was crowned the U.K.’s second-most visited city in 2015, surpassed only by London, as approximately 4.05 million visitors headed to Edinburgh - domestic and international combined (source: Edinburgh Tourism Action Group)

Increased popularity among both domestic and international visitors has, unsurprisingly, created investor demand in the Edinburgh hotel sector. A decade ago, an average of 11,070 rooms were available daily, and as of July 2019 the city offers 16,170 hotel rooms – a 46.1% increase in supply.