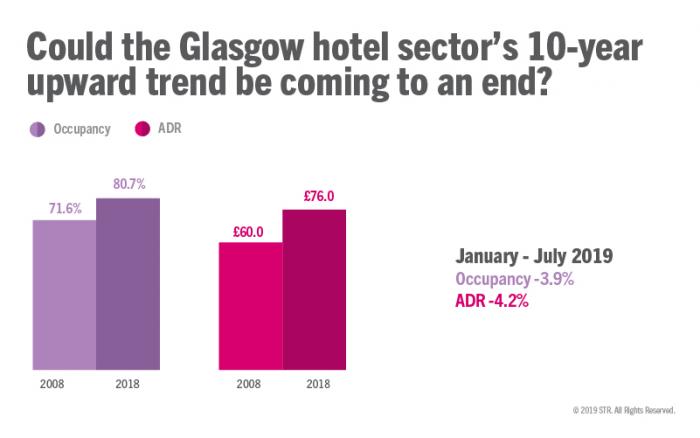

Glasgow

Glasgow, with a population that surpasses Edinburgh, also attracts large scale events, concerts, conferences and festivals that create significant demand. The market’s popularity has also attracted investors and created an extensive pipeline of hotels that include notable new entrants to the market.

Over the past 19 months (2018-July 2019), eight new hotels have opened, adding more than 1,000 rooms. A variety of properties entered the market, offering an aparthotel, serviced apartments, and Midscale to Upper Upscale options to Glasgow’s broad spectrum of visitors. There are currently 2,204 rooms across eight pipeline projects that are scheduled to open between August 2019 and the end of 2020 - the majority of these will be associated with global hotel chains. If we look at the last ten years, Glasgow saw a 22.0% rise in room supply.