Previous MRM versions: 17 April | 24 April

Week ending 1 May

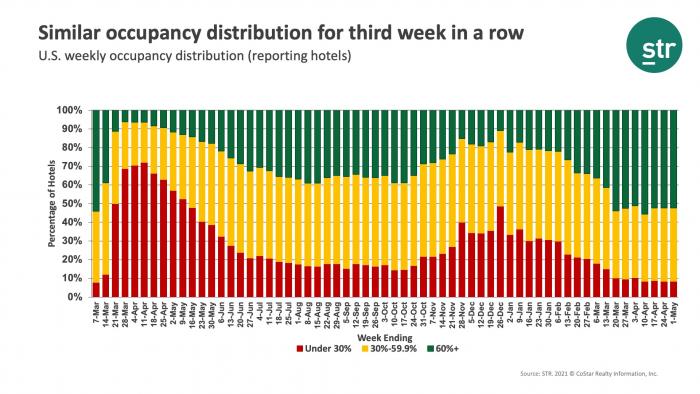

For a third week, U.S. hotel occupancy remained just above 57% and 54% on a total-room-inventory basis (TRI), which accounts for temporarily closed hotels. Room demand fell slightly with the weekly level staying above 21 million for a seventh consecutive week. A closer look revealed that room demand dropped during the weekdays and increased over the weekend. Weekend occupancy advanced week over week to 71%, with room demand up 1.1%. Notably, Saturday’s room demand was the highest recorded since 15 February 2020 with occupancy at 73% (69% TRI).