Previous MRM versions: 10 April | 17 April

Week ending 24 April

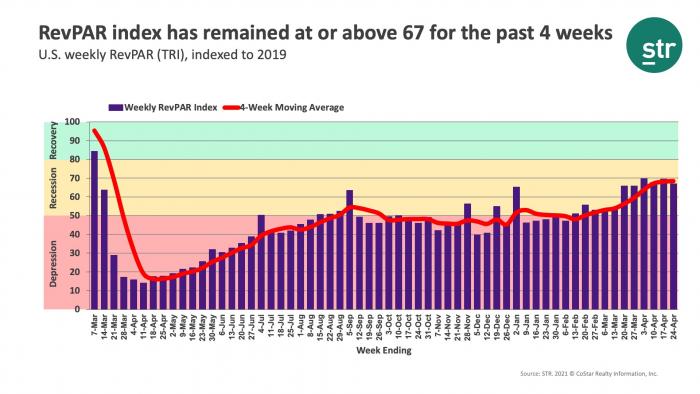

Hotel performance growth appears to be on hold when compared with the solid gains seen during the spring break period. In a week-over-week comparison, U.S. hotel occupancy was flat during 18-24 April at 57.3%. On a total-room-inventory (TRI) basis, which includes temporarily closed hotels, occupancy was 54.4%. Weekly room demand increased slightly and remained above 21 million for a sixth consecutive week.

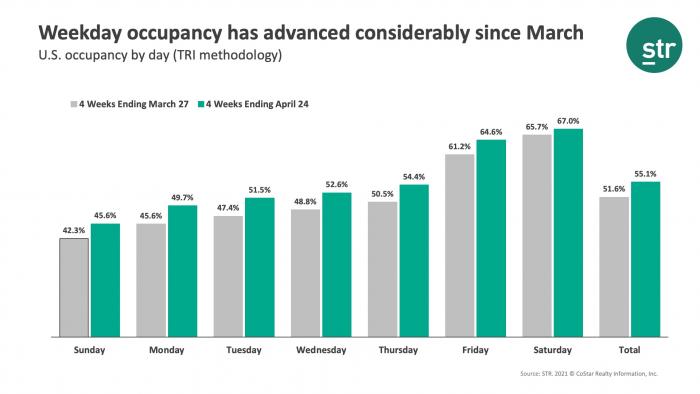

Like in the previous week, weekend occupancy was above 70% (67% TRI). The emerging story is the gain in weekday occupancy, which has been growing steadily over the last month. In reviewing the room demand growth in the past four weeks versus the previous four weeks, weekday demand increased an average of 16% over the period versus a 10% increase on weekends.