Previous MRM versions: 3 April | 10 April

Week ending 17 April

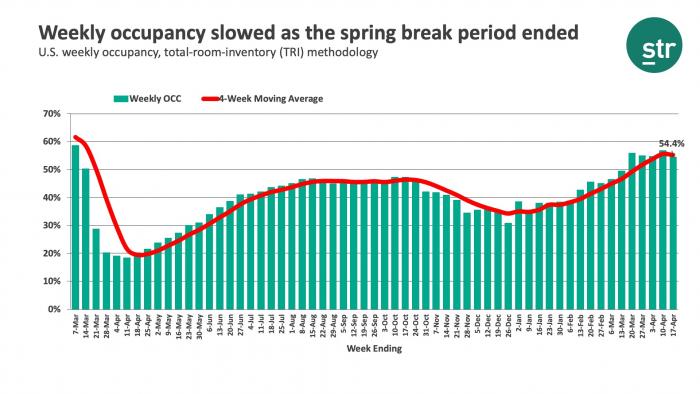

As expected, due to the end of the spring break leisure season, U.S. industry recovery came to a pause during the week ending 17 April as demand fell 4% week over week. The good news, room demand remained above 21 million for a fifth consecutive week. Occupancy for the week was 57.3% using STR’s standard methodology and 54.4% on a total-room-inventory (TRI) basis—the latter accounts for temporarily closed hotels.