Previous MRM versions: March 20 | March 27

Week Ending 3 April 2021

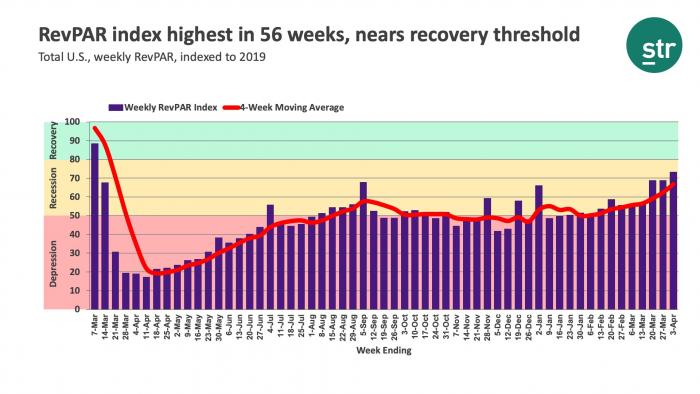

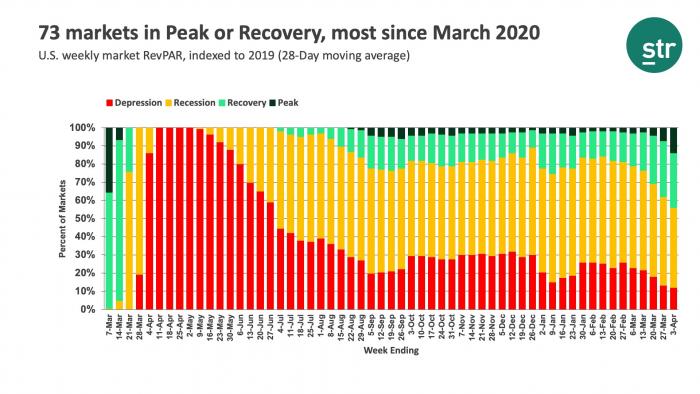

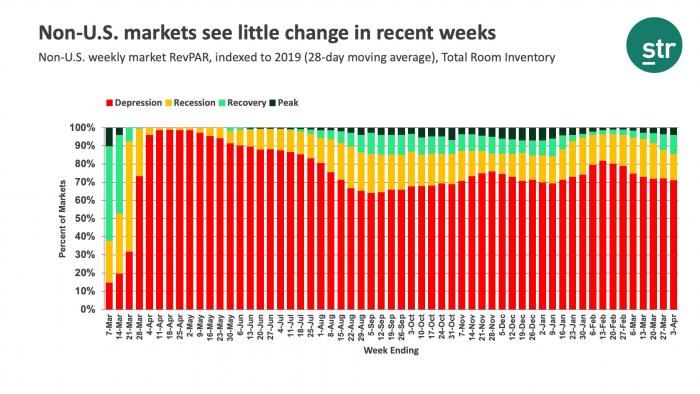

Weekly RevPAR rose to US$65.34, which was a 4.2% increase week over week and the industry’s highest level of the past 56 weeks when indexed to 2019. RevPAR has increased week over week all but three times this year. STR’s Market Recovery Monitor reflected the country’s stronger overall RevPAR performance with 73 markets either in Recovery or Peak categories. More encouraging, only 20 markets were in the Depression category, the least of the past 53 weeks. Top 25 Markets are also improving, and as a group, entered the Recession phase for the first time. However, most of the markets that are classified as in Depression continued to be those in the Top 25, including San Francisco, Boston, Washington, D.C., New York City, and New Orleans. Of all U.S. markets, those five markets had the lowest RevPAR when indexed to their 2019 benchmark. Similar trends were noted when using STR’s total-room-inventory (TRI) methodology. RevPAR on this basis was $61.76, up 3.7% with 67 markets in the Recovery or Peak categories.