Are you tracking the Market Recovery Monitor each week? Utilizing data and benchmarking to navigate recovery will be a key focus of the 2021 Hotel Data Conference. Click here for registration, with both in-person and virtual options available for our 13th annual event in Nashville.

Previous MRM version: 3 July | 10 July

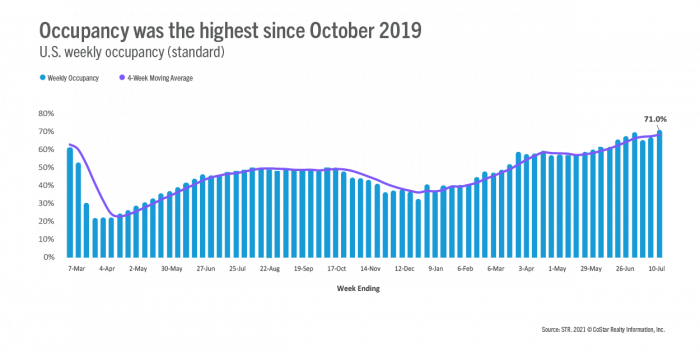

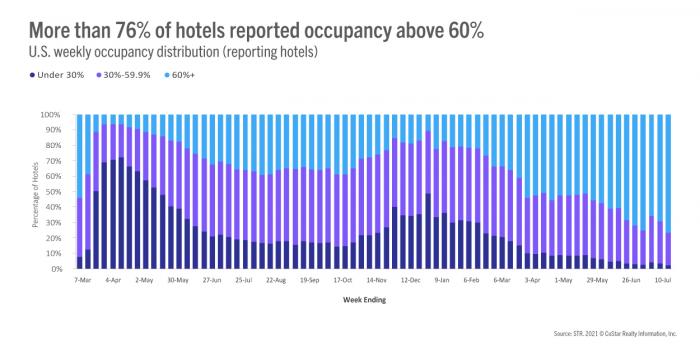

In the week ending 17 July 2021, occupancy soared to 71.0%, its highest level since the Columbus Day holiday week of October 2019. Also for the first time since the week ending 19 October 2019, daily occupancy was above 70% Wednesday through Saturday. Weekend occupancy surpassed 80% for the second time this year but was shy of the high recorded four weeks ago. Excluding STR’s Top 25 Markets, occupancy was 72% and was the best since late summer 2019. Small (under 75 rooms) and medium (75-299 rooms) hotels did even better with occupancy of 73% for the week. More than one-fifth of all reporting hotels had occupancy above 90%, which was the most since summer 2019 but still fewer than the 27% at or above that level during the corresponding week last year. On a total-room-inventory basis (TRI), which accounts for temporarily closed hotels, weekly occupancy was 68.2%.