Previous MRM versions: March 6 | March 13

Week Ending 20 March 2021

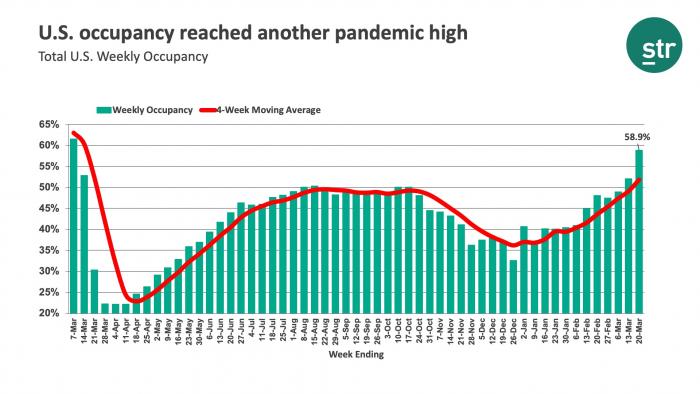

Pent-up demand has clearly revealed itself over the past two weeks. Over the 14-day period ending with 20 March, U.S. hotel demand reached 21.8 million room nights, which was an increase of 3.7 million from the previous two weeks and the highest for any two-week window since late February/early March of 2020. As a result, occupancy hit yet another pandemic high of 58.9%. Even when switching to STR’s total-room-inventory (TRI) methodology, which factors in those properties temporarily closed due to the pandemic, occupancy still came in at 55.7%. Occupancy, regardless of methodology, has been on a steady rise since late January.