Previous MRM versions: 15 May | 22 May

Week ending 29 May

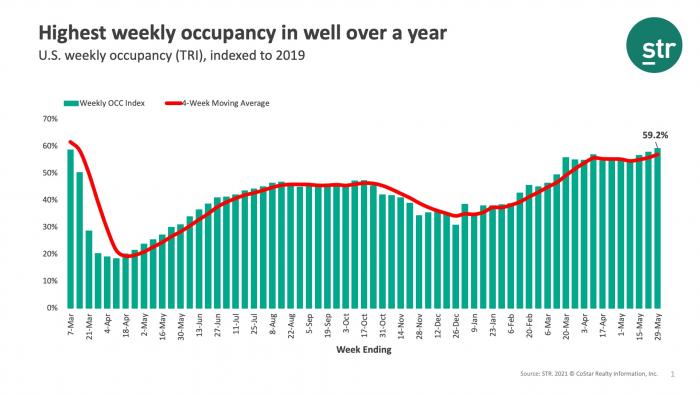

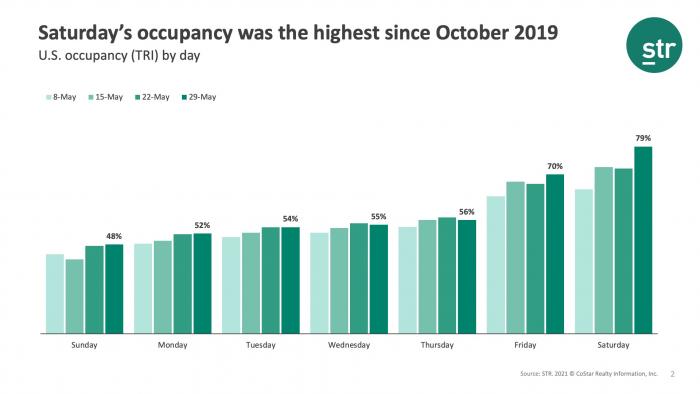

As anticipated, the Memorial Day weekend ushered in the highest occupancy the U.S. industry has seen since the start of the pandemic. For the week ending 29 May 2021, weekly occupancy reached 61.8%, the highest level since the final week of February 2020. On a total-room-inventory basis (TRI), which accounts for temporarily closed hotels, occupancy was 59.2%, which was also the highest since the pandemic’s start. During the first two days of the Memorial Day weekend, occupancy topped 78.3% (74.9% TRI), the highest weekend occupancy since October 2019. The weekend accounted for nearly all the week-on-week increase in occupancy as weekday occupancy was flat versus the previous week. Saturday saw the largest week-on-week jump, reaching nearly 83% (79% TRI).