Previous MRM versions: 1 May | 8 May

Week ending 15 May

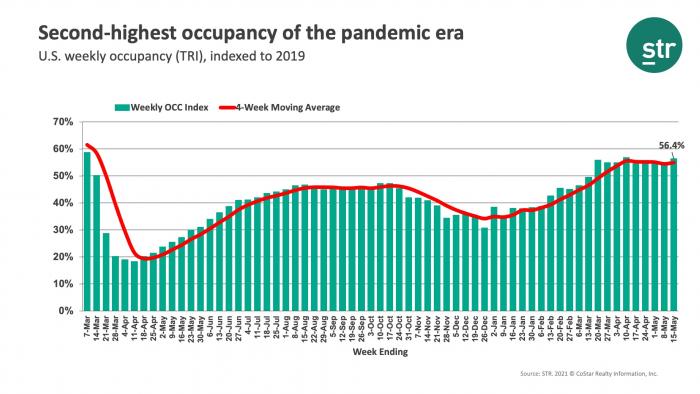

Signs late last week pointed to a negative performance impact from the hacking of the Colonial Pipeline and resulting gas shortages. Crisis averted, however, as U.S. hotel demand, occupancy, ADR and RevPAR all reached or were near pandemic-era highs. Further, all four measures hit pandemic highs when looking strictly at the weekend. Occupancy for the week averaged 59.1% or 56.4% on a total-room-inventory (TRI) basis, which accounts for temporarily closed hotels. That occupancy was the second- highest level of the past 62 weeks. Weekend occupancy was 73.6% (70.2 TRI), the highest level since Valentine’s Day weekend in 2020.