Previous MRM versions: March 13 | March 20

Week Ending 27 March 2021

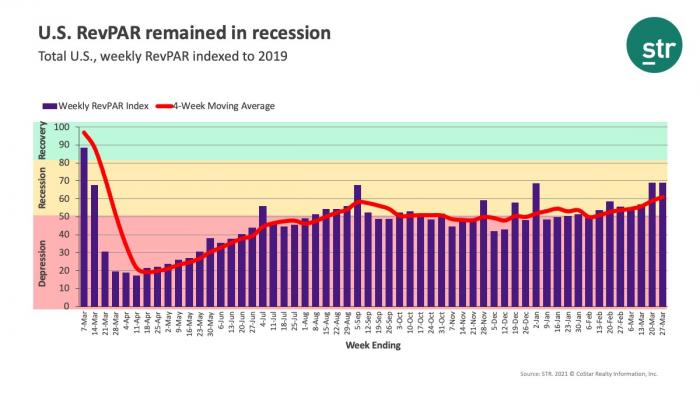

With Spring Break waning, it wasn’t surprising to see performance slow a bit in the week ending 27 March. Room demand, which was 350,000 less than the week of 20 March, was still above 21 million for a second straight week. Before the week of 20 March, that level had not been seen since before the pandemic. To put the demand change in perspective, on average, each U.S. hotel sold 10 less rooms this week than in the previous one. This week’s demand level was 83% of the level attained during the comparable week in 2019.

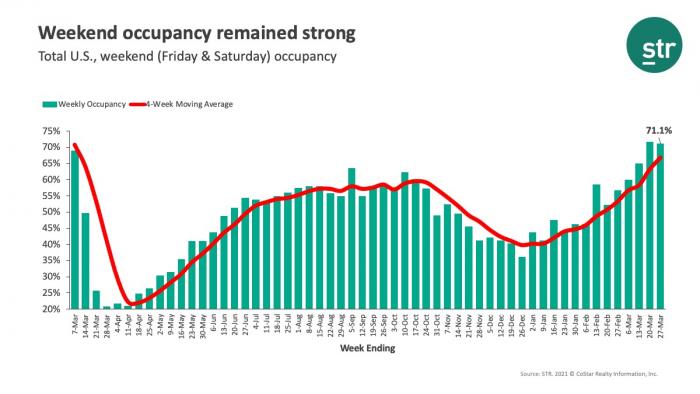

Weekly occupancy was 57.9%, down 1.1 points from last week. A closer look revealed that weekday demand, particularly on Wednesday and Thursday, held back industry performance. However, weekend occupancy (71.1%) remained strong and only slightly weaker than the previous week. Of note, Saturday’s level (73.4%) was the third highest daily occupancy of the past 15 months.