Previous MRM versions: 22 May | 29 May

Week ending 5 June

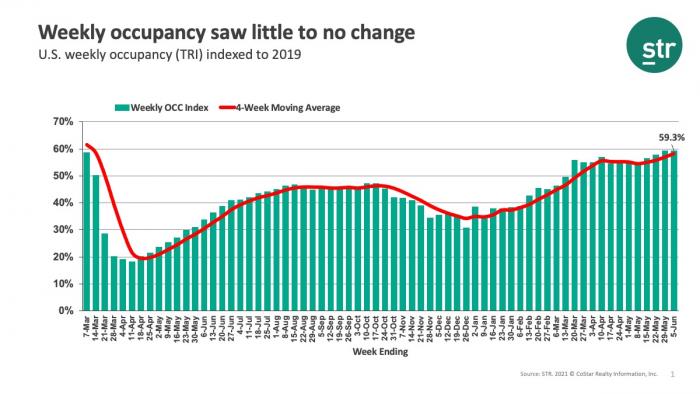

For the week ending 5 June 2021, U.S. industry occupancy increased ever so slightly to 61.9%, up +0.2 points from the previous week. Room demand increased for a fifth straight week but by its smallest amount of the past four weeks. Supply was also on the rise as more hotels reopened ahead of the summer season. The increase in weekly supply (16,000 rooms) shaved off 0.1 points from weekly occupancy. As of 8 June, there were 402 hotels (96,000 rooms) still closed in the U.S. with 46% of all temporarily closed hotels in just three markets: New York, Orlando, and Chicago. On a total-room-inventory basis (TRI), which accounts for temporarily closed hotels, weekly occupancy was 59.2%, flat from the previous week.